U.S. residential property prices have risen sharply in recent years and, consequently, the same upward movement has been seen in rents. As a result, many investors who follow the U.S. real estate market have been surprised month after month by the strength of the segment in the country.

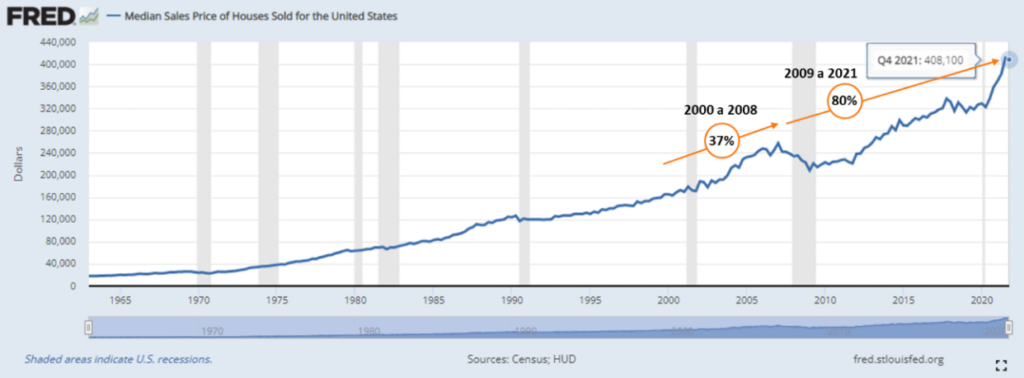

The chart below, which shows the median prices of homes sold in the country, in nominal values, illustrates this movement. While from 2000 to the price peak in 2008 the appreciation was 37%, from the 2008 peak to the end of 2021 the appreciation reached 80%.

After the decline following the 2008 crisis, a considerable increase in the prices of properties traded in the U.S.

Much of this strength is attributed to variables such as low interest rates for home purchases (in effect until a few months ago) and the government's generous financial aid package to combat the effects of the pandemic. These are certainly important factors to consider. There is, however, a structural reason for this surge: a lack of supply.

The long-term fundamentals for the rise in residential property prices

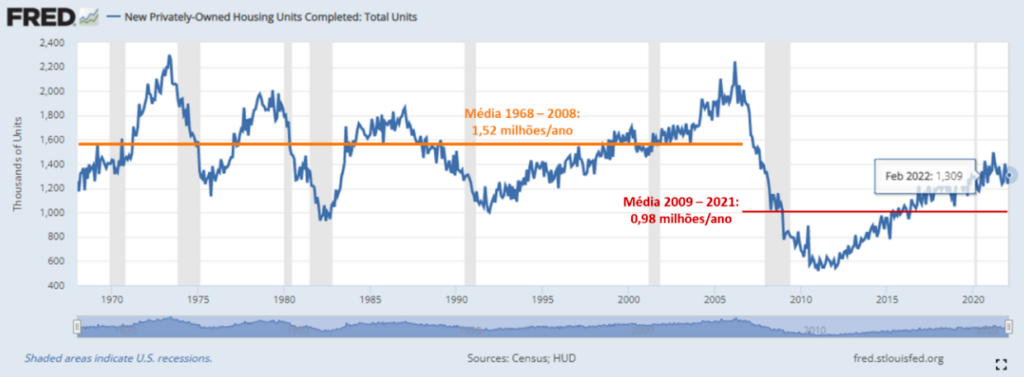

As can be seen in the chart below, which represents the annualized number of residential units delivered to the market each quarter, from the 1960s until 2008 there were always periods of supply expansion and contraction. Despite this, the average delivery each year was 1.52 million units during that period. This level of supply was sufficient to maintain a certain balance in the residential market, meeting growing demand and replacing obsolete properties.

Historical series with quarterly, annualized data on deliveries of new residential units in the U.S.

What we saw after 2008 was an abrupt drop in the construction of new homes, to the lowest level in the historical series, culminating in the delivery of just 565 thousand new units in 2010. Thus, from 2009 to February 2022, the annual average of new residential unit deliveries was 980 thousand units, a value substantially lower than in the four preceding decades.

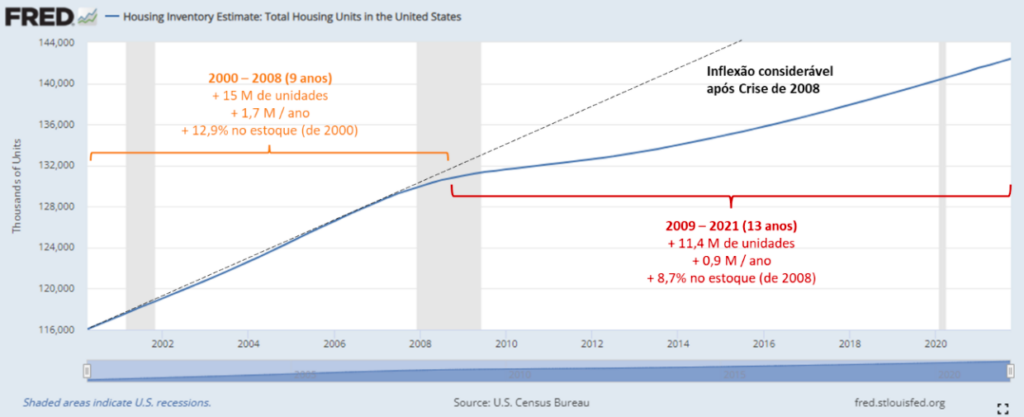

In the chart below, which displays the total stock of units in the United States, the inflection after 2008 is evident. While in the 9 years from 2000 to 2008 about 15 million new units were added to the housing stock, in the following 13 years, from 2009 to 2021, only 11.4 million units were added to that stock.

Evolution of the residential unit stock in the U.S.

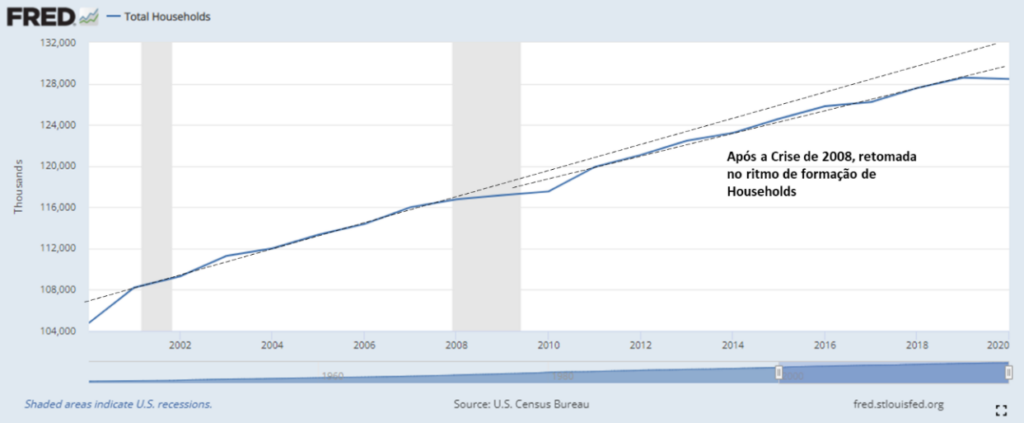

As can be seen in the chart below, the 2008 crisis also had an impact on the formation of households (the group of occupants of the same property), since any economic crisis can, for example, postpone marriage plans or children moving out of their parents' homes — factors that normally drive demand for new housing. However, from 2010 onward, the pace of growth in the number of households returned to what it was in the pre-crisis period, restoring normal levels of demand growth.

Evolution of the number of households: a fairly subtle inflection after 2008

Consequences of the imbalance

Given the imbalance between supply and demand of residential units in various states across the country, with a production volume below what was needed for several years, as well as the slow recovery in the construction sector, four effects, well documented by data, became evident:

- An increase in U.S. residential property prices, as shown in the first chart;

- An increase in housing rental values;

- A general decline in vacancy rates in the residential segment;

- A reduction in capitalization rates (cap rates) in the residential segment.

Conclusion

With the recent rise in U.S. interest rates, purchasing power for U.S. residential properties should decline and, therefore, the upward movement in prices should ease. On the other hand, the annual supply of new U.S. residential units is still below the historical average, not to mention the construction deficit of the last decade and cost inflation in the sector. Thus, contrary to what is speculated, the rise in prices and rents in the U.S. residential market is not a passing phenomenon. It may lose momentum, but it should persist for a few more years.