While recent conflicts between nations and the pandemic drove poverty in some regions of the world, the resilience of the economic elite became evident in the recent results of companies focused on high-end segments, such as personal luxury goods, luxury cars, boats and private jets. Surprisingly, these niches not only withstood the crisis but also posted notable growth, revealing shifts in the consumption preferences of high-income or high-net-worth individuals.

Between 2017 and 2022, a significant global increase was observed in the number of individuals considered “high-net-worth” – with net worth above US$1 million – with growth of 42%. In addition, “ultra-high-net-worth” individuals, with net worth above US$ 30 million, experienced a similar increase, rising 44% over the same period, according to Knight Frank.

In the personal luxury goods market, the Louis Vuitton Moët Hennessy (LVMH) group stands out, owner of prestige brands such as Louis Vuitton, Dior, Tiffany and Hennessy, surpassing a market value of 500 billion dollars in 2023, driven by the accelerated rise in sales during the pandemic.

In the automotive sector, the global microchip shortage limited the supply of cars, leading automakers to prioritize quality over quantity to offset the decline in sales. The growing demand for cars, as an alternative to public transportation, further fueled demand. These two factors, combined with the increase in the higher-purchasing-power audience, generated strong growth in the luxury segment, and the luxury car market is projected to grow 14% annually through 2031, according to McKinsey.

While airlines suffered drastically during the pandemic, the private jet segment posted considerable growth, driven by the cutting of commercial routes, which limited travel between countries, and by the preference to avoid prolonged contact with other people in enclosed spaces.

For the real estate market, the story was no different. The increase in time spent at home, due to lockdowns and mandatory remote work, led people to rethink their housing habits, seeking larger spaces, more rooms, amenities and outdoor areas. In addition, people began to consider moving to cities that would allow for a higher quality of life, seeking to balance a healthy lifestyle with remote work.

This dynamic, together with the expansionary monetary policy adopted by the Fed, caused home purchase prices and rental values in the U.S. to rise considerably, heating up the market. Subsequently, however, the market cooled, with the increase in the benchmark interest rate and mortgage rates.

Although the more niche high-end real estate market tends to follow patterns similar to the broader real estate market, the fluctuations proved particularly favorable for the luxury segment after the pandemic.

The following data, compiled by Redfin, compares the luxury segment with the rest of the market, defining luxury homes as properties above the 95th percentile in market value within their respective metropolitan regions, while non-luxury homes are those properties between the 35th and 65th percentile of these markets.

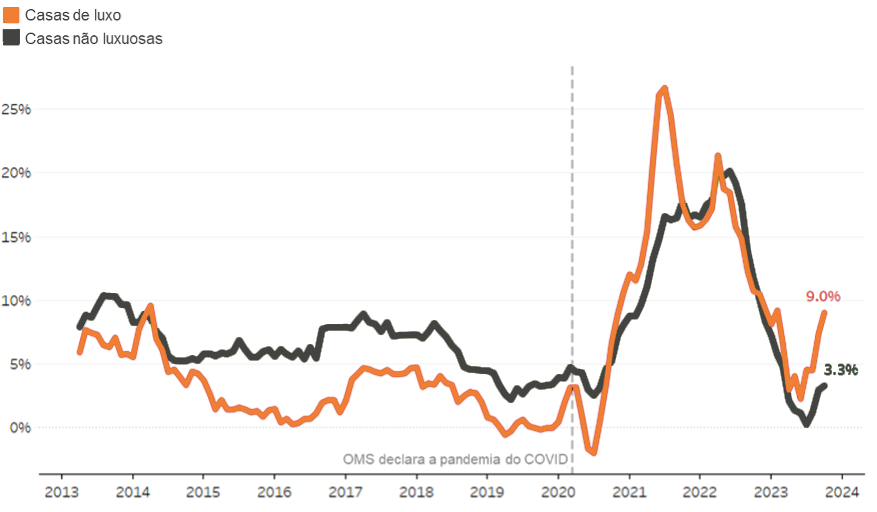

Median home sale price (year-over-year change)

As can be observed, in terms of annual price growth between 2013 and 2020, the performance of the mid-tier market was even better than that of the luxury market, in part due to the general shortage of supply in the U.S. residential market.

From 2020 onward, during the pandemic, there was sharper growth in high-end home prices and, after the slowdown in 2022 and 2023, this segment is recovering more vigorously, with luxury home values rising nearly three times as much as the mid-tier market.

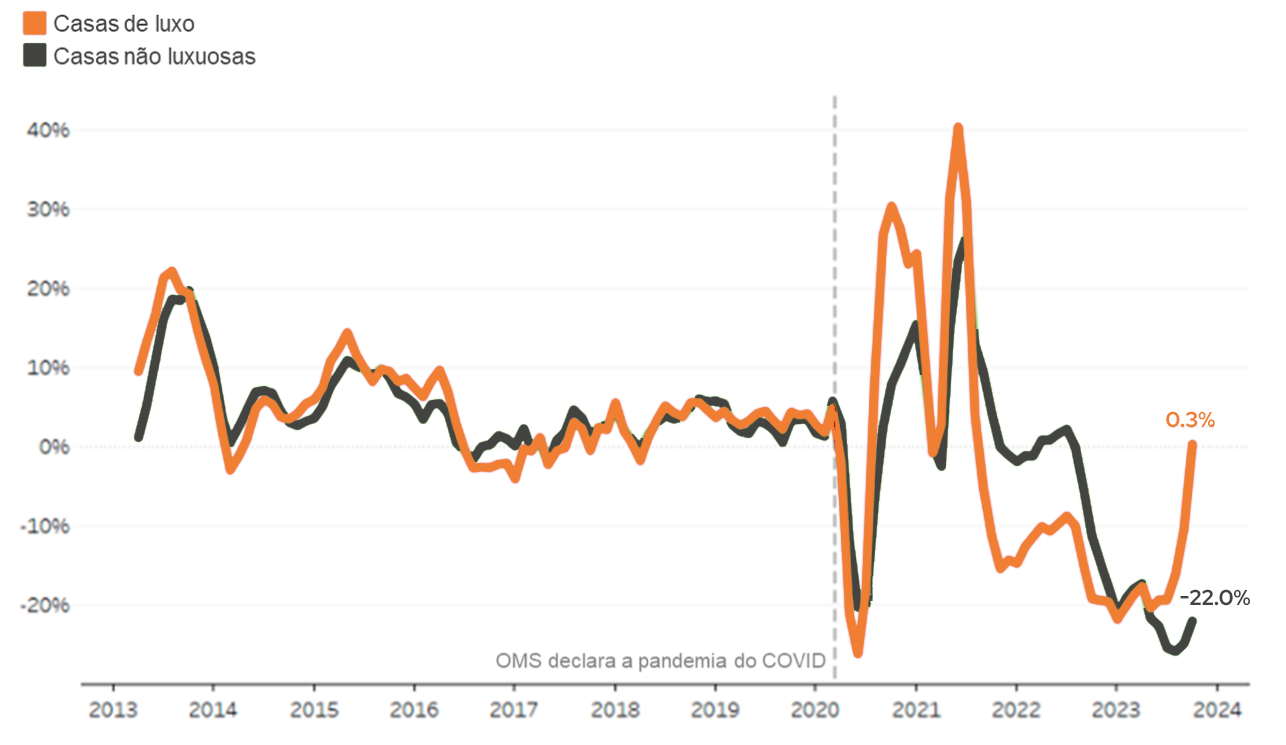

The number of luxury properties listed for sale also experienced a higher peak during the pandemic, followed by a subsequent reduction. Currently, this segment registers a slight increase in listings compared with the prior year, while other properties continue in steep decline.

Number of homes listed (year-over-year change)

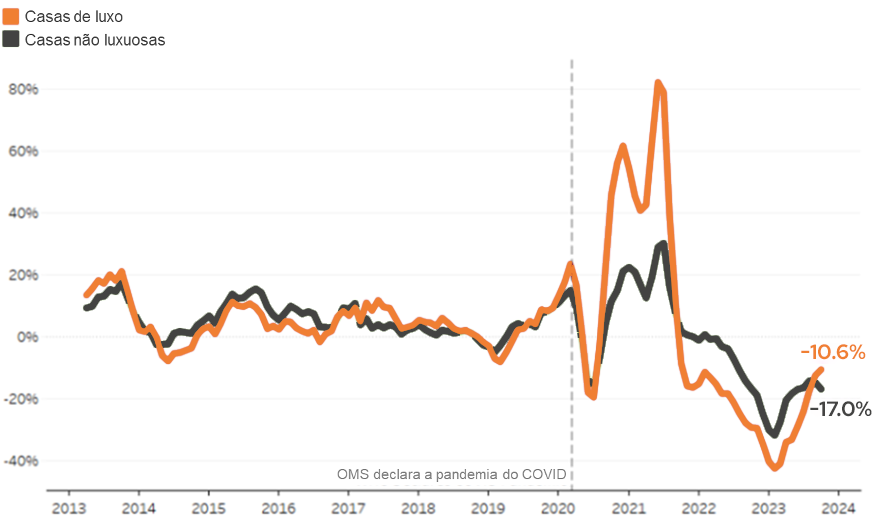

Similarly, the sales volume of high-end residences saw notable growth of 80% in 2021 and, like other properties, faced a decline in the following two years. Currently, this index shows signs of recovery, with the luxury market presenting a less pronounced decrease compared with the other group of homes.

Number of homes sold (year-over-year change)

Although no segment is immune to crises, several factors explain why the high-end real estate market proves more resilient in more adverse economic moments:

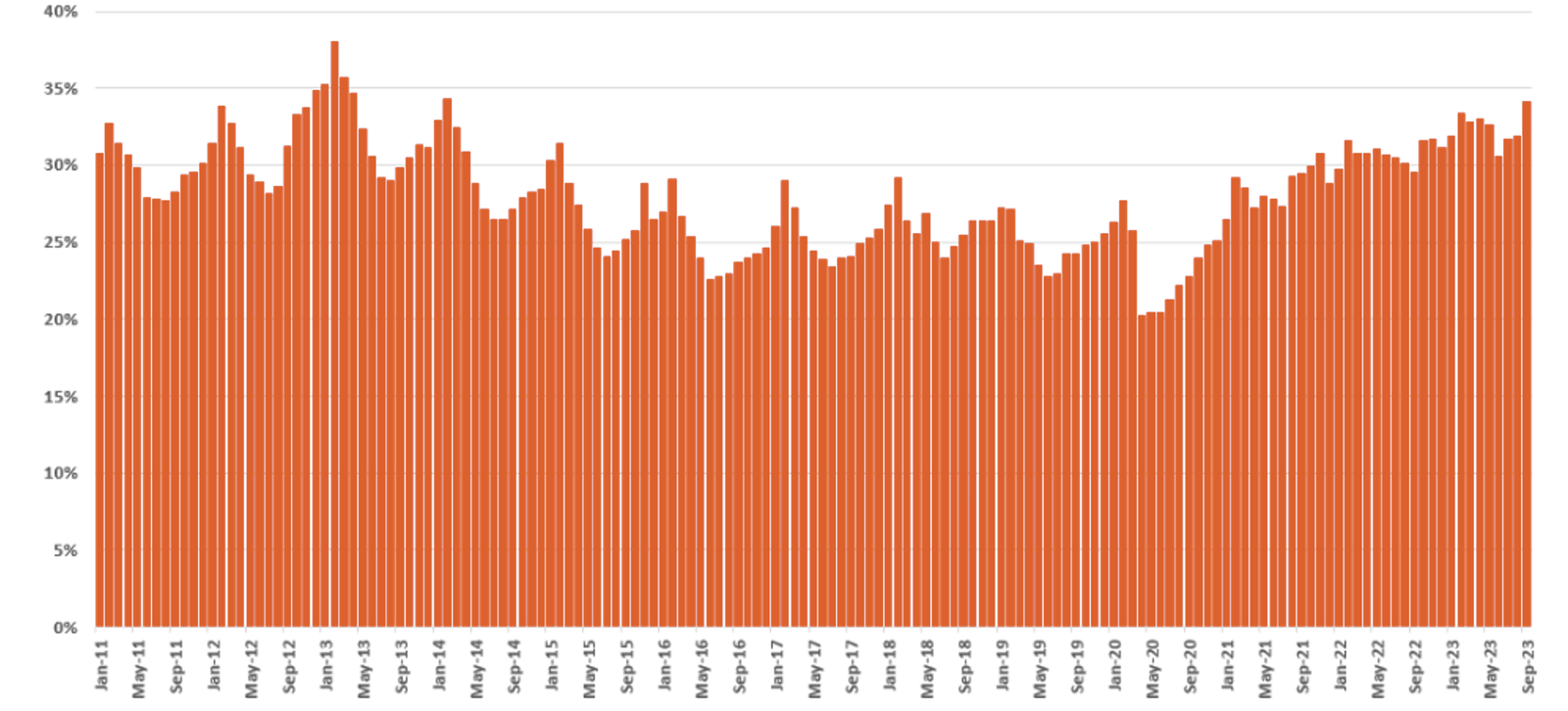

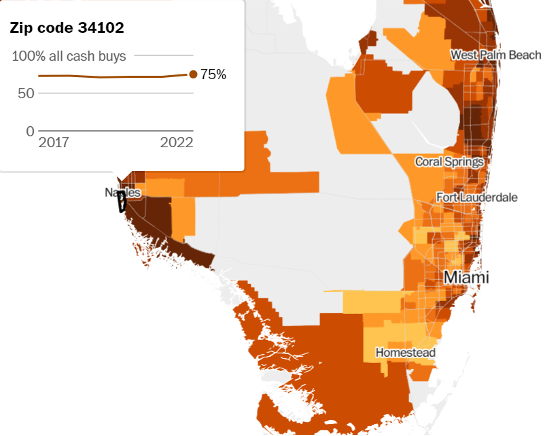

- This type of product is designed for an audience with high purchasing power, able to acquire properties outright, without the need for a mortgage. According to Redfin data for the market as a whole, about 35% of all homes acquired in Q3 2023 were purchased in cash (“all-cash transactions”). For luxury homes, this figure rises to 42%, versus only 28% of properties not considered luxury.

In specific markets, such as Naples (FL) and West Palm Beach (FL), known for the strong presence of high-income buyers, between 60% and 75% of acquisitions are made in cash, depending on the area of the city. Thus, despite mortgage rates having reached their highest level in 23 years, this phenomenon has little effect on this market segment. In addition, buyers with high purchasing power can pledge other assets in their portfolio as collateral for loans, gaining access to more attractive interest rates.

Percentage of homes acquired entirely in cash in the U.S.

Percentage of homes acquired entirely in cash in South Florida

- Properties in the best locations are considered long-term investments, characterized by low price volatility, safety and stability. A survey by Knight Frank indicates that one third of the total wealth of ultra-high-net-worth individuals is allocated to real estate, directly or indirectly.

- The exclusive profile and broad range of amenities of these properties, combined with the limited supply of land in select regions, make luxury real estate considered strong status symbols, which is highly desired by economic elites.

Despite the impacts of the pandemic on certain economic segments, the luxury real estate market demonstrated remarkable resilience. With the rise in high-net-worth and ultra-high-net-worth investors, this sector, like other high-end markets, is expected to maintain favorable prospects in the coming years, standing out as a resilient long-term investment amid a more volatile economic landscape.

New American markets most desired by the elite

According to Philip White, President and CEO of Sotheby's International Realty, in addition to the traditional markets sought by the American economic elite, such as New York, some new markets in the country have drawn considerable interest from this audience:

- Florida: The absence of a state income tax, the pleasant climate and the extensive coastline, with various amenities, have driven high demand for luxury properties in cities such as Naples, Tampa, West Palm Beach and Cape Coral.

- Texas: Similar to Florida, this state benefits from the absence of a state-level income tax and from a strong pro-business environment. The cities of Austin and Dallas are centers of great interest.

- Colorado: Proximity to nature and outdoor activities are the main attractions. Boulder, near the Rocky Mountains, and Aspen, famous for its ski slopes, are the cities in greatest demand.

- Wyoming: As in Colorado, nature plays a highly influential role. The Jackson Hole area is the epicenter, situated near Yellowstone National Park and one of the best-known ski resorts in the United States.