The year 2022 was marked by a few “black swans” and considerable volatility: war, an energy crisis, high global debt, inflation and successive interest rate hikes, just to name a few.

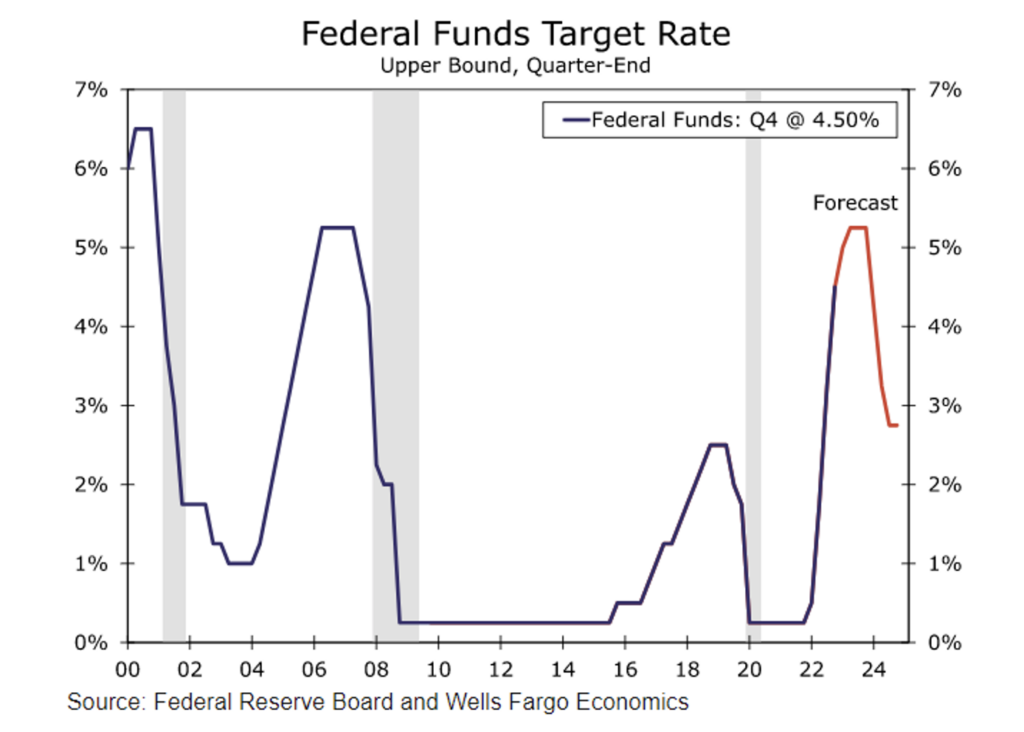

In macroeconomic terms, in the United States, Wells Fargo published in its latest report the expectations that investors can have for 2023: a moderate recession from the second half of the year, with GDP estimated to fall by 1%, and rate hikes peaking in May at the 5.00% - 5.25% level. The start of the economic recovery would begin as early as the beginning of 2024.

The importance of alternative assets in portfolio diversification

This scenario, combined with strong turbulence in traditional markets, is turning alternative investments into “THE” alternative. A recent survey by SS&C, one of the world's largest administrators of Hedge Funds and Private Equity, shows that 70% of investment managers intend to increase their allocations to alternatives in 2023. And, in addition, the expected growth of this market as a whole over the next 5 years is 71%, jumping to more than US$ 23 trillion globally.

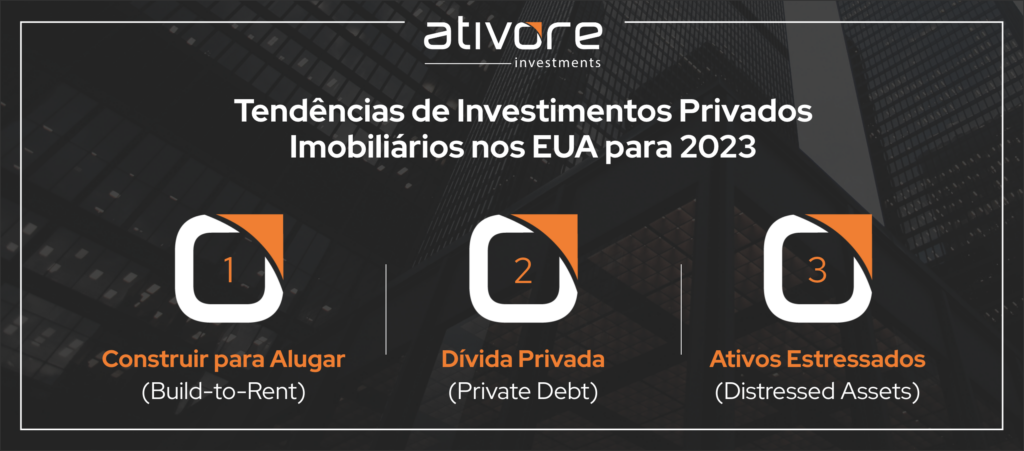

Trends in the U.S. real estate market for 2023

In this article, we will discuss a few trends to support the decision-making of both individual investors and institutional investors seeking diversification in hard currency in the U.S., while keeping a certain distance from the noise of the major media and the volatility of the more traditional markets. They are:

Context: the U.S. residential market and its different investment strategies

Before discussing the first trend, “Build-to-Rent,” it is necessary to provide context on the different moments being experienced by the sub-niches of the residential market. There is a lot of talk about the “Housing Market,” but it is a broad and sophisticated market, with completely different risks and opportunities depending on the segment chosen for investment.

The U.S. residential market is the largest in the world, and it is estimated that the total combined value of residential properties was close to $44 trillion in 2021, according to an analysis by Zillow. The vast majority of these properties are Single-Family Properties, residential homes built to be purchased (the Build-to-Sell thesis), mostly by individuals (families).

2023 Is not the year for the “Build-to-Sell” thesis (Build-to-Sell) for Single-Family Properties

in the U.S.

This is a segment that already began to suffer in 2022, and the trend is for it to continue this way through at least 2024. The reality is that the sharp interest rate increases promoted by the Fed to contain inflation in the U.S. generated two side effects that impacted this market simultaneously:

1. Demand and the pace of construction of “homes for sale” (Build-to-Sell) plummeted

Naturally, with the sudden and aggressive increase in the cost of buying a home, demand for Single-Family Properties was also impacted. Data from Cushman & Wakefield show that over the past year, the number of tenants in their properties moving out of renting to buy their own home fell by about 35%.

In addition, according to a recent Wells Fargo report, the expected decline in the pace of construction of new Single-Family Homes is 21% in 2023, a very significant reduction considering the size of this market.

2. It became very, very (!) expensive for a family to stop renting and buy their own home

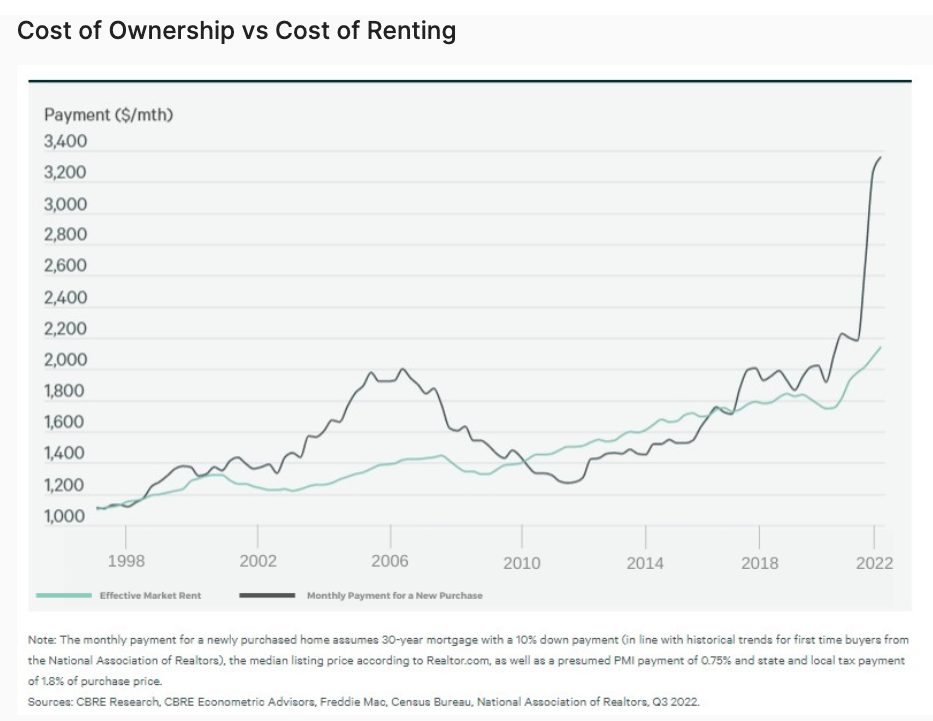

Mortgage financing rates went from approximately 3% per year to 7% per year over a span of about one year. The chart below, which compares the cost of buying with the cost of renting a home, demonstrates on its own the impact this brought to American families.

Some say that rent is already too expensive, which varies considerably depending on the region in which this information is analyzed. But the fact is that the average price of rents currently relative to the average household income stands at 22%. For reference, HUD considers that a tenant is “paying too much” (or Cost Burdened) when this indicator is above 30%.

To get an idea of the real consequences of this, according to a recent study by Cushman & Wakefield, it is currently, on average, US$ 471 more expensive per month to cover the cost of paying principal plus interest on a mortgage than to rent a similar property (without considering the down payment, in the case of a purchase). It is the largest difference in history. Not long ago, the norm was for rent to be about $65 more expensive; that is, in relative terms and considering the current moment, the choice to rent has never been so easy (or necessary).

While buying a home becomes increasingly difficult, renting ends up being, by far, the best option for American residents, which keeps demand—already strong—even more resilient. Add to this the continuous increase in the number of families, the very low supply of new homes between 2010-2020 and the obsolescence of older properties, and one concludes that, both on the supply side and on the demand side, the Build-to-Rent thesis is in fact more appropriate than the Build-to-Sell thesis at this moment. The article “Fundamentals of the Appreciation of Residential Properties in the U.S.” illustrates some of the points discussed here.

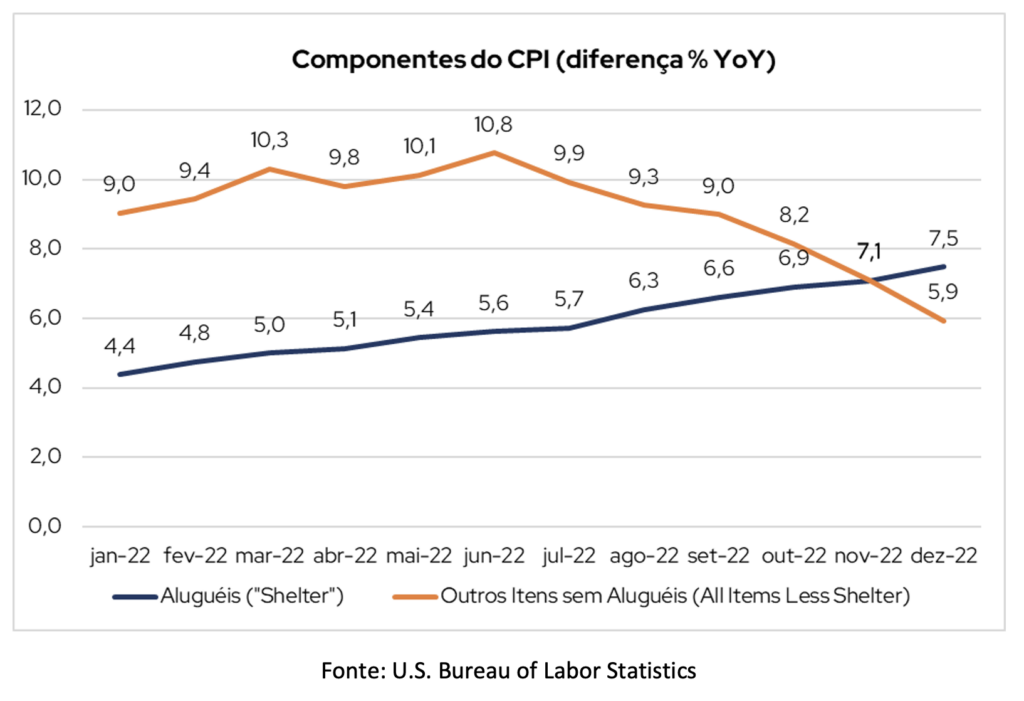

To corroborate this analysis, see the chart below, which shows the components of the Consumer Price Index (CPI) for rent inflation (“Shelter”) and for all other items except rents (“All Items Less Shelter”). Even after the Fed's efforts to contain price increases, rent inflation continues to grow. We discuss this phenomenon, as well as the risks tied to the thesis, in detail in the article “The Fed's Challenges in Containing Inflation and the Opportunities for Real Estate Investors in the U.S.”.

In a scenario of potential recession and high volatility, the major banks and financiers of real estate projects reduce their appetite, increase bureaucracy and the time it takes to grant credit, and end up hindering the viability of new projects—even those aligned with the current market environment and presenting a diligent and feasible business plan.

This “mismatch” of traditional banks with the current context is, in fact, a “feast” for Private Debt operators, especially those niched in certain asset classes and/or regions, and that have a greater focus on Senior Debt—that is, with priority over the other layers of the asset's financing and, consequently, more conservative.

This reality translates into safe investment opportunities, while at the same time offering good returns, and this occurs basically for two reasons:

1. With the limited supply from large financial institutions, the pipeline of new loans increases considerably in the private market.

As one of the classic forms of remuneration for an operator (and consequently for its investors) are the fees charged when the debt is originated and, at the end, when the debt is paid off, the more “turnover” the pipeline has, the more the investors' potential return increases—especially in diversified private debt funds, which may hold dozens/hundreds of loans at the same time, bringing not only greater returns but also safety through the spreading of risk.

2. Since the interest charged by operators in this market grows as U.S. interest rates rise, investors' potential return also ends up benefiting.

It is worth noting that the risk also ends up being greater, since the cost of debt also increases, but it is controlled to the extent that one invests in the most Senior layer of the financing. That is, should the asset go into default, the property is taken over at discounts between 30% and 40%, making it a win-win situation—whether through the higher return driven by rising interest rates, or in the case of default where the property is recovered at a very low cost, maintaining, and sometimes even increasing, investors' returns.

At the last “PERE America Summit” conference, Richard Barkham, Global Chief Economist at CBRE, one of the largest Real Estate firms in the world, stated in his opening remarks: “we might be seeing a once-in-a-generation pricing opportunity,” that is, one of those windows of opportunity that appear only once every few decades.

The rationale behind this statement makes sense and is, in fact, the other side of the coin of trend 2 explained above. This is because, at the same time that loans granted diligently by private, niche operators in a senior position can bear good fruit, they can also be the cause of problems for players in the real estate sector that took on more debt than they could and/or should have, bringing another type of opportunity for managers and professional investors who are capitalized to take advantage of the moment.

Interest rates - the main stress factor in the current market

Properties do not always become distressed due to poor management; often it is exogenous factors, beyond the control of real estate operators, that end up forcing a sale at a lower price than in a standard market scenario. Take the example of Covid-19, where hotels went to zero occupancy “overnight,” a premise impossible to predict.

Even though it was market consensus that interest rates would rise at some point, the speed of this was a premise in projects to be validated over time. And what happened? Interest rates rose significantly, very quickly, causing the cost of debt to soar in certain real estate assets and significantly increasing the potential for stress.

It is worth noting that even good assets, selected diligently, in good regions and with first-rate operators, can suffer in atypical situations like the current one. However, they obviously have a much better chance of weathering the turbulence and recovering fully.

Stress for some, opportunity for others

The sharp and abrupt increase in interest rates may therefore be, in 2023, a factor generating opportunities at discounted (distressed) prices not seen in a long time, with some situations being more conducive to this occurring. They are:

(1) properties that have variable-rate financing without a “cap” (upper limit on the interest rate) or with a “cap” maturing in the very short/short term, and that will have considerable difficulty renewing the “cap” or refinancing the property;

(2) properties that have fixed-rate financing whose interest-only payment period (interest only) is maturing or about to mature, and that will see a significant increase in debt service with the payment of principal as well. The difficulty of refinancing at current interest rates may force a discounted sale.

(3) properties financed at variable rates, with a “cap” in effect over the next 2-3 years, but that have reached the ceiling of that “cap” (maximum cost of debt) and where the asset is not performing as expected, generating negative cash flow.

Analyzing and exploring each of the cases above would easily make for a new article, but the most important thing at this moment is to keep in mind that any property that needs new debt (refinancing) or needs to renew its interest rate “cap” will have to have exceptional operational performance, a very low leverage percentage (less than 60%) and/or a very comfortable cash position so that there is no stress on the asset.

The market has already shown some signs that this trend may in fact

materialize in 2023

Ativore's partner operators, both in the residential segment and others, have spotted opportunities to acquire distressed assets. One of them recently signed a contract to buy three Multifamily Properties in Texas from a seller whose variable-rate financing “cap” is expiring. In the Self Storage market, we are analyzing the possibility of generating IRRs close to 14% per year, in dollars, with zero leverage—something absolutely uncommon in the U.S. real estate world.

Conclusion

Ativore, through its funds, is capitalized to take advantage, in early 2023, of unique investment opportunities in the Build-to-Rent segment and recently approved a new Private Debt asset for the private investor portfolio. In addition, we are proactively analyzing the Self-Storage, Strip Malls, Medical Office Buildings, Office (in specific regions) and Hotel (leisure-oriented) markets. Other classes, despite the caution, will also be considered for investment as long as they have the correct underwriting (due diligence).

It is our relationships (which cover practically the entire U.S. territory), experience, technical tools and ability to structure international portfolios that will be decisive for the selection, analysis and allocation decisions throughout 2023.

Although we present some trends that may occur in the market in 2023, it is always good to remember that the “beauty” of the real estate market is that good acquisitions can be made in any region or niche, and at any moment in the cycles, given that each transaction is unique, with singular negotiation drivers that will determine the chances of success of that investment.

At the end of the day, it is impossible to predict exactly what will happen and how each market will react, but acting diligently, creatively and intelligently in such a broad and complex market is what will increase your chances of generating good returns, safely, even in moments of high volatility. Count on us.

Bibliographic references

- https://www.cushmanwakefield.com/en/united-states/insights/us-articles/sky-high-mortgage-rates-benefitting-multifamily

- https://privatebank.jpmorgan.com/gl/en/insights/investing/todays-us-real-estate-dilemma-buy-build-sell-now-or-wait

- https://wellsfargo.bluematrix.com/links2/html/a9a4e05a-bb13-4578-b79e-20be2fbfc9a6

- https://www.cushmanwakefield.com/en/united-states/insights/10-critical-questions-for-2023?

- https://www.zillow.com/research/us-housing-market-total-value-2021-30615/

- https://login.iintoo.com/US/pub/news_posts/1iamztuy?login=1&_hsmi=240563895&_hsenc=p2anqtz-_dtvvh1ph5lm653ajwxab3qegpebm5j8cnllh6zw-ozbk_btaasos4t1zrhk3055nymmpojphqjy-1hkp6sk7ixwbf6a

- https://zain-ventures.com/real-estate-trends-2023/

- https://www.schroders.com/br/br/schroders-brasil/visao-de-mercado/mercados/outlook-2023---ativos-privados-tres-areas-de-foco-em-tempos-desafiadores/

- https://www.wsj.com/articles/rising-interest-rates-hit-landlords-who-cant-afford-hedging-costs-11673900169