Two events marked the past week in the United States: (1) the outcome of the Fed meeting (the U.S. central bank) and (2) the release of November inflation, measured by the CPI (Consumer Price Index). With respect to interest rates, the increase came as the market expected, with a 0.5% rise, to the 4.25%–4.50% range, putting an end to the consecutive 0.75% hikes.

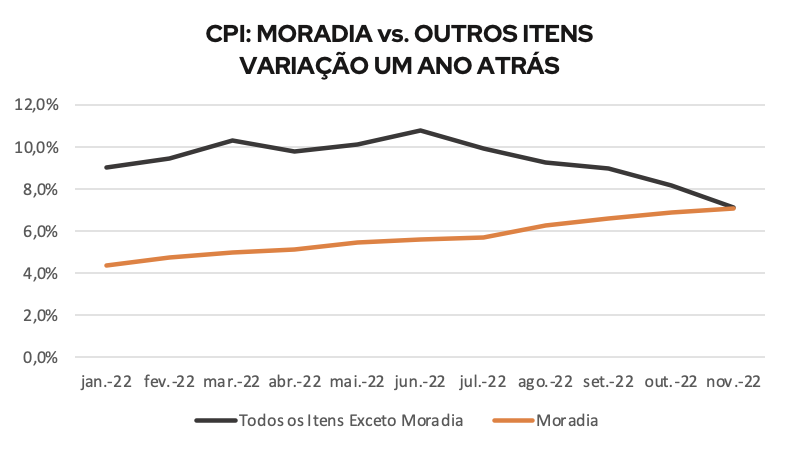

Inflation, in turn, showed that it continues firmly on its deceleration path, reaching 7.1% in November, after hitting a peak of 9.3% in June and 7.7% in October. In his speech, Jerome Powell made clear that the Fed's goal is to bring inflation back down to the 2% level, acknowledging that rates will remain higher until that happens.

For this to happen, the item with the greatest weight in the CPI calculation, the "Shelter Index," which measures the evolution of residential rent prices, must also enter a deceleration path, and this is the main challenge the Fed will encounter in the U.S. real estate market. Some of the reasons for this are:

- Rent prices carry the greatest weight among all CPI items, and they continue to rise, even after the successive interest-rate increases carried out by the Fed.

- Rents were already under pressure due to structural gaps between supply and demand in the residential market, recently addressed in an article written by Ativore (as can be seen here).

- Now, with the interest-rate increases carried out by the Fed to combat inflation, other side effects are putting even more pressure on rents.

This challenging context for the Fed has reinforced one of the investment theses that is a focus of Ativore's committee for 2023: build-to-rent.

The goal of this article is to give the reader a deeper understanding of the challenges the Fed will face in taming inflation in the residential market, and how this context benefits this investment strategy, which represents one of the main alternatives for investors who are seeking to reallocate resources internationally and/or are suffering in other, more traditional asset classes.

To guide the reader through this construction, the text has been divided into three parts:

- How the CPI is calculated and how the Shelter Index (Housing) affects the price-formation index in the U.S.;

- Details on the challenges the Fed will face, specifically in the U.S. real estate market, to control inflation;

- How this context contributes to reinforcing the build-to-rent thesis over the next 1–2 years, until the price index is under control.

Part 1 – understanding the Consumer Price Index (CPI) and the weight that the Shelter (Housing) item carries in its calculation

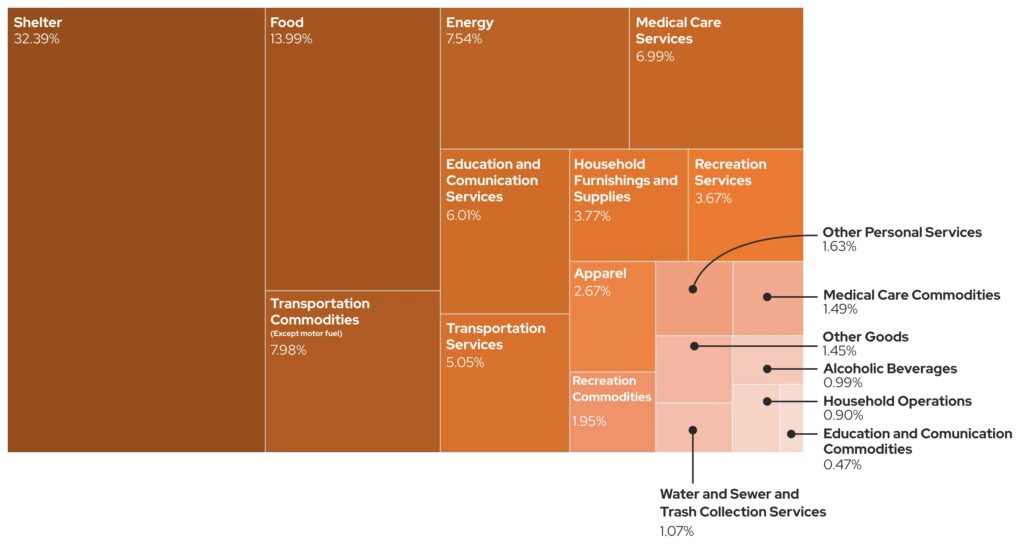

1.1 Composition of the U.S. price index (CPI)

The CPI is composed of a basket of products and services, with "Housing" being the item with the greatest weight — by far — in this calculation. This is clear in the diagram below, where "Shelter" (Housing), with about 33% weight, has more than double that of the second item, "Food," with 14%. The difference is even greater when the comparison is made against all the other elements:

1.2 Details on the "Shelter Index" (Housing), and why we cite "rent prices" when we refer to it.

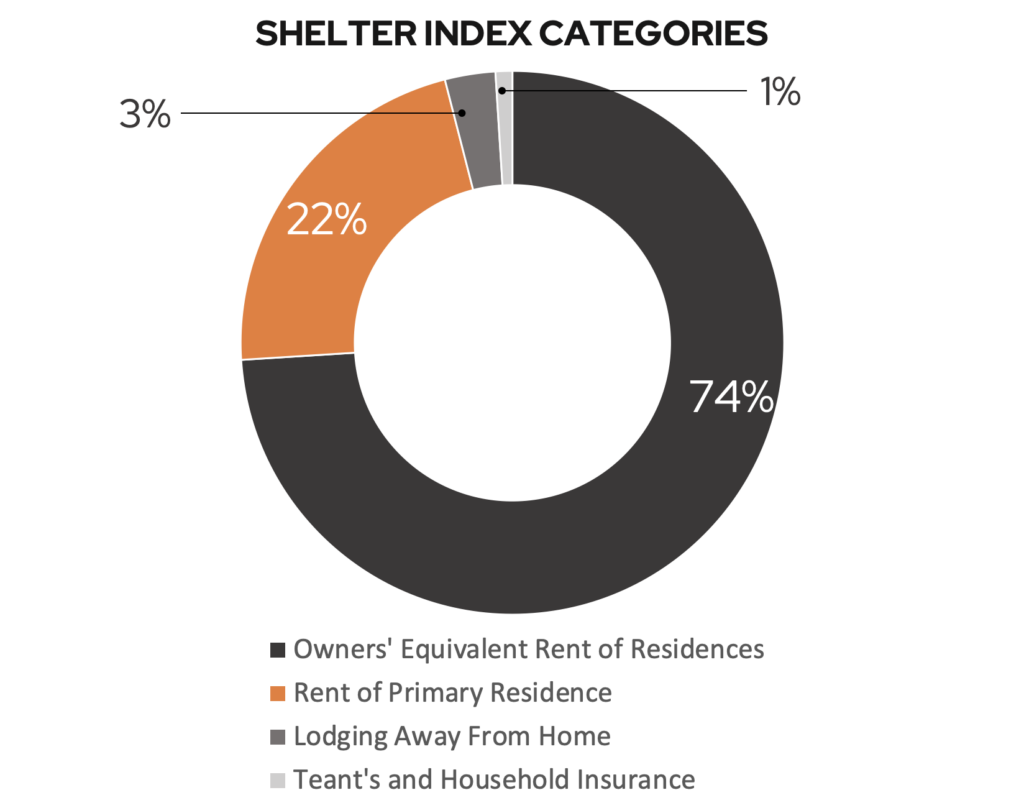

The Shelter Index, which as we saw above accounts for the largest portion of the inflation calculation, is measured through 4 subdivisions, with 96% of the weight being in two of them:

- Owner Equivalent Rent (74%) – this is how much a given property owner would pay in rent for a similar residence.

- Rent of Primary Residence (22%) – this is the rent actually paid by tenants for their homes.

- Lodging Away From Home (3%) – prices of hotel and inn rooms.

- Tenants and Household Insurance (1%) – prices of insurance for residences.

Interestingly, the CPI does not take into account the variation in property prices themselves, since it treats them as investments, using only rental values for the purpose of calculating the "Shelter Index," whether through the estimated rent for a given property (Owner Equivalent Rent) or the rent actually charged to tenants (Rent of Primary Residence). For this reason, on several occasions throughout the text we are referring to this item as "rents," or "rent prices."

Part 2 – why controlling inflation necessarily requires "taming" rents as well and, therefore, why this is the Fed's great challenge with respect to the U.S. real estate market?

As we observed earlier, rents carry great weight in the formation of inflation, and despite the clear signs of CPI deceleration, which has already fallen 23% since June, this did not occur because of rent prices. On the contrary, rent prices are in fact still (!) rising, even after the Fed's efforts to contain inflation through the consecutive interest-rate increases.

And why do rents keep rising?

Beyond the insufficient supply of residential properties (the subject of an article written by Ativore recently, cited earlier), which had the largest gap in U.S. history over the past 12 years and was already exerting strong inflationary pressures, the recent interest-rate increase – used by the Fed as a tool to combat inflation – generated two side effects:

- It pushed a significant portion of the population into renting, by making it harder to access credit for home purchases and;

- It has inhibited countless construction initiatives, further reducing the projected supply of residential properties.

Part 3 – how does this context reinforce the build-to-rent thesis?

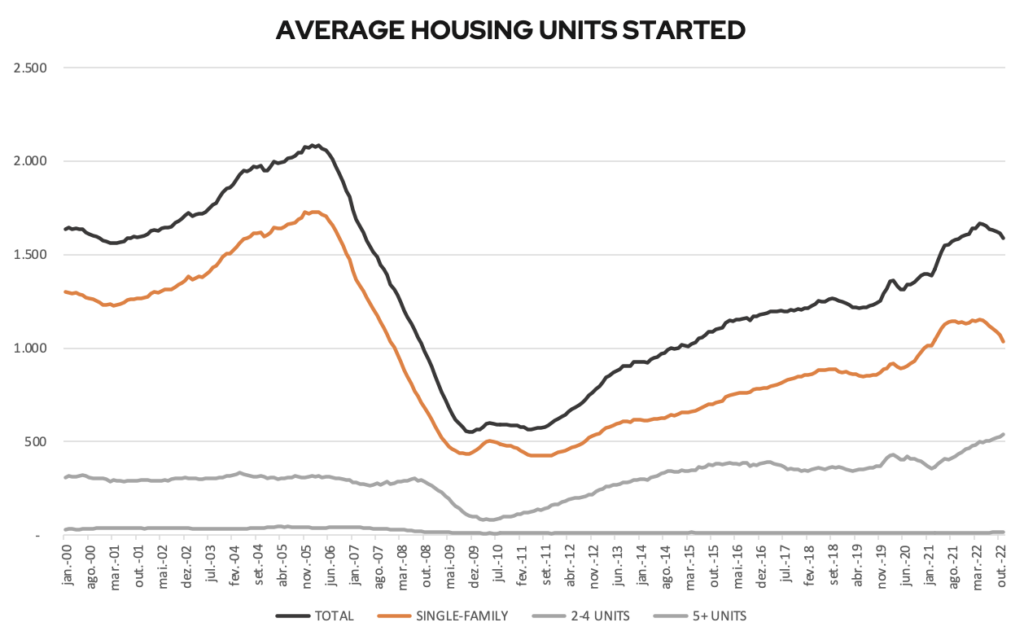

The construction of Single Family Properties Build-to-Sell — that is, single-family homes geared toward sale to the consumer, and not for rental — has plummeted recently (orange line).

The construction of Multifamily Properties (gray line), multifamily buildings that are exclusively geared toward rental and that benefit from the current inflation, continues at a good construction pace. This is justified by the reduction in supply, which worsened with the sharp drop in home construction, at the same time that a larger share of the population needs to rent, since financing for purchase is inaccessible to a good part of the population due to the rise in interest rates.

For this reason, the need to control inflation, while simultaneously meeting very strong demand for new homes, opens an opportunistic window for applying the build-to-rent thesis {link}, provided it is done professionally and in observance of the countless nuances that such projects present.

What precautions should you take before investing?

To invest in this market, deep and specialized knowledge is required, as there are several factors to consider, some of them being:

- "Location, Location, Location." There are regions (macro and micro) with strong barriers to entry and restricted supply, while others may be saturated due to ease of construction and/or being the focus of the moment.

- Entry prices, determined by the "Yield on Cost," must be analyzed very cautiously, so that their returns and cash flows remain resilient even with new interest-rate increases.

- Another item of utmost importance is the financing structures, which must also have protection mechanisms (hedge), in the current scenario of rising rates.

- Post-construction rent projections must be made prudently, considering that at some point over the next 1–2 years, rents will stabilize at normal growth levels.

- Stress/sensitivity tests must be even more conservative, modeling investment results on the premise of a negative Shelter Index (falling rents) for one or more quarters of recession, verifying the robustness and viability of the projects in more extreme scenarios.

Conclusions

- Rents in the residential market have a high impact on the formation of the "Shelter Index," which in turn carries the greatest weight in the CPI calculation, the U.S. inflation index.

- For this reason, to control inflation, it will also be necessary to "tame" the "Shelter Index" (rent inflation). With interest-rate increases alone, the path will be far more arduous, and it will also be necessary to increase the supply of rental properties.

- With high interest rates, the tool used by the Fed to combat inflation, two undesirable phenomena emerged as a side effect:

- construction of Single Family Properties Build-to-Sell plummeted.

- a significant portion of the population was pushed into renting, because they could not obtain mortgages at the rates currently in effect.

- Both of the items above continue generating inflationary pressure on rent prices, and they further add to the supply gap that already existed, and which on its own already caused rent inflation, making it even harder to reduce the "Shelter Index."

- An increase in supply is necessary in the current context

- on the demand side, which was already high due to the supply gap, and which will remain robust for longer on account of a larger share of the population renting

- on the supply of new home construction, which had been reduced over the past 12 years following the 2008 crisis and was showing signs of recovery, but recently plummeted again after the interest-rate increases.

- as a tool to combat inflation, because without new construction, it will be even harder to reduce rent prices

- Therefore, with fewer market players building, with fewer people able to buy properties, and with very strong rental demand, the build-to-rent thesis as opposed to build-to-sell presents a great opportunistic window for the next 1 to 2 years.

The Fed has a great challenge ahead; however, the moment also brings opportunities to more professionalized investors. For this window to be properly seized, it is necessary to count on professional operators and managers who understand the current dynamics and deeply know each of the markets in which they operate.