Anyone who invests in the financial markets knows how important it is for a portfolio manager to be able to adapt to market changes and even take advantage of them to capture certain investment opportunities. In the U.S. real estate market, it is no different.

Economic environment and impacts on the U.S. real estate segment

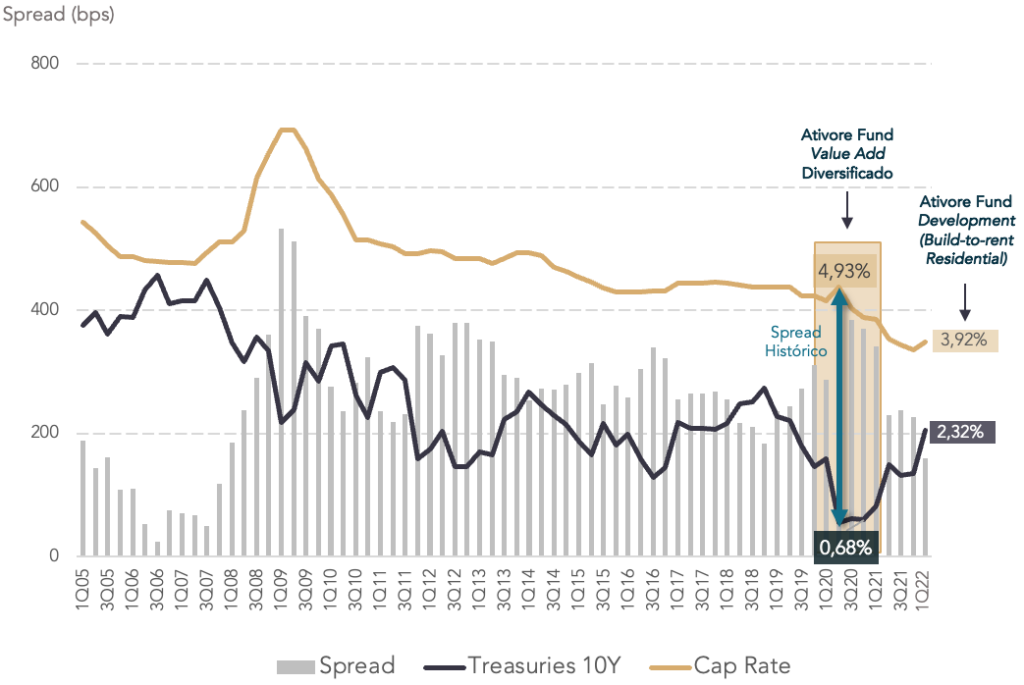

Between 2020 and 2021, taking advantage of the post-COVID market distortions that resulted in wide spreads between U.S. interest rates, at all-time lows, and property capitalization rates (cap rates), which were quite high, we invested in operating (already leased) properties, acquired at prices below replacement cost and financed at very low rates, which has generated quite attractive returns for our clients.

Interest rate spread in the multifamily market

Since the beginning of 2022, however, the shift in the market fundamentals observed over the previous two years has been clear. Property prices rose in response to the low-interest-rate environment and investor appetite for the residential segment and, consequently, market cap rates compressed, causing the potential returns to be captured in operating assets, that is, those already leased at the time of investment, to decline.

Building residential real estate in the United States for rent (residential build-to-rent)

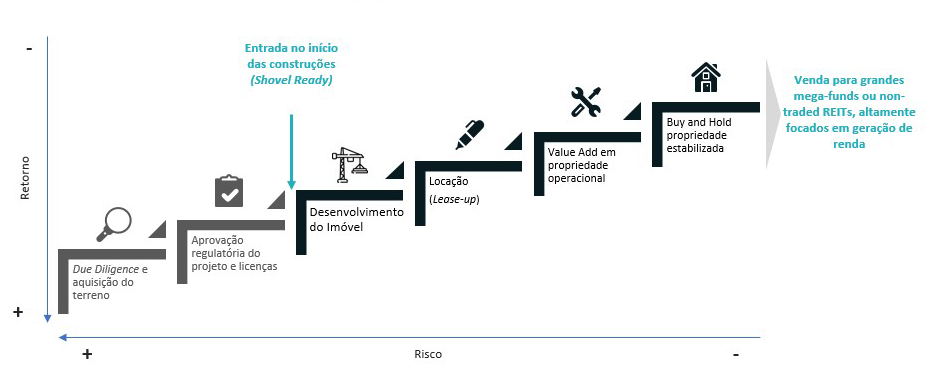

Within this same environment, however, a new opportunistic window emerged. This time, one step back in the real estate value chain, in the construction of residential properties intended for rent (residential build-to-rent).

Compared to operating projects, build-to-rent projects also prove to be proportionally less susceptible to the negative impact of rising interest rates on their financing structure, since the level of leverage is traditionally lower and the contribution of financing to the total return of the investment is much smaller.

On the other hand, we understand that investing in properties from the construction stage carries additional risks for investors compared to investing in operating properties that generate cash flow, and for that reason, when designing the investment strategy it is very important to have risk mitigants in place that only an experienced operator in the U.S. build-to-rent market can provide.

Stages of real estate development

As managers, we believe that by knowing the markets where the housing deficit is most acute and adopting the right mitigants, it is possible to explore build-to-rent opportunities with an excellent risk-return profile!