The scenario of rising inflation in the U.S., globally and in Brazil

The global economy, after having passed the peak of the pandemic and shown signs of recovery, finds itself in a moment of strong uncertainty once again. The main source of concern at the moment is inflation, which is affecting not only more fragile economies but also mature and normally more stable ones.

If it was initially thought that inflation was a passing phenomenon, the result of governments' aggressive stimulus policies in response to the pandemic, today it is almost unanimously viewed as a more persistent phenomenon, caused by rising commodity prices — especially energy — and by the disruption of various global supply chains.

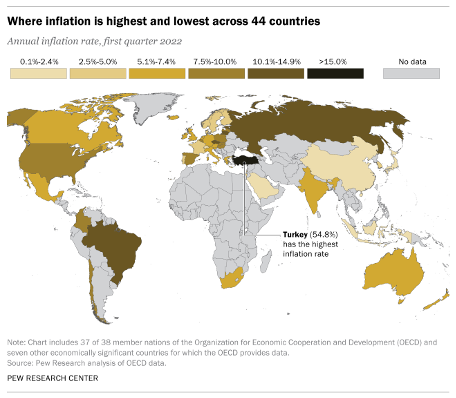

In the eurozone, annual inflation, measured between April 2021 and May 2022, reached 8.1%, including stable countries such as Germany, which had 7.9% inflation in that period. This, however, is a global phenomenon, as can be seen in the figure below.

In the U.S., the CPI (Consumer Price Index) posted growth of 8.6% from April 2021 to May 2022, which represents the highest rate in the last 40 years, as can be seen in the chart below.

Trailing 12-month CPI since 1982

If inflation is alarming in developed countries, in Brazil the scenario is far from encouraging. From April 2021 to May 2022, inflation reached 11.6%. The difference is that, here, despite the Central Bank's efforts, the government's commitment to bringing inflation back to the center of the target seems much less evident.

In addition, 2022 is an election year and neither of the two candidates leading in the polls is particularly inclined toward fiscal austerity. In both candidates' speeches, there is no shortage of references to granting raises to public servants, tax exemptions and increases in spending — generally with direct proposals, including ending the spending cap.

Thus, if the global situation is one of uncertainty, in Brazil the situation is even worse, with a less rigid government effort to combat rising prices, and inertial inflation once again worrying economists.

Real estate investment as protection against U.S. inflation

In an attempt to contain rising prices, central banks around the world have been raising benchmark interest rates, which tends to depreciate asset prices across the board — a phenomenon strongly felt in equity and crypto-asset markets, for example. Other assets, such as real estate, tend to be comparatively better positioned since, in most cases, for properties acquired with the goal of renting, there is a good ability to pass inflation through to tenants. Particularly in the U.S., the net effect of inflation on residential property prices over the long term tends to be positive, since there is a structural shortage of housing supply that, combined with rising inflation, tends to positively impact rents. This factor, combined with rising construction costs, should keep property prices under pressure (which does not mean that, in the short term and in the event of a sharp economic slowdown, the prices of these properties could not be impacted by rising interest rates).

In an article in Valor Econômico in March of this year, Pedro Barreto, Chief Strategist at Ativore, addresses the strategy adopted by the company for wealth protection against inflation, via investment in U.S. Real Estate Private Equity (link). One of the key points of this strategy is the ability of real estate to adjust its revenues at a pace similar to inflation.

In this sense, although all types of real estate achieve some level of protection against inflation, some classes can pass on rising costs more quickly than others, ensuring that their real returns are not eroded by rising prices. This ease is mainly tied to the characteristics of each segment of the real estate market, which make lease agreements shorter or longer. Thus, the shorter the leases, the easier it tends to be to adjust to inflation. Below is a brief explanation of how each type of asset positions itself along this spectrum.

- Hotels are the assets that can pass on inflationary increases most quickly, able to adjust the price of their nightly rates and related services (food, beverages and other amenities, such as spa) daily as costs rise.

- Self-storage facilities come next, with monthly contracts with their tenants.

- Multifamily and Senior Housing properties follow, with leases of three months to one year, on average.

- Retail properties usually have leases lasting more than two years. In these cases, there may be clauses providing for annual rent escalations following U.S. inflation, which needs to be investigated before investing.

- Office sector properties also have longer leases (generally five years or more) with the possibility of contractual escalations, but with greater bargaining power for tenants, to offset the longer commitments.

- Finally, there are Industrial class assets. These properties generally require heavier construction work to accommodate a new tenant and are part of a distribution network, so leases tend to be longer, lasting ten years or more. Thus, escalations may be less frequent and the ability to adjust must be analyzed case by case.

Ease of pass-through does not eliminate the need for robust analysis

Although the ease of passing on prices is an important component for wealth protection, it is possible to find investment opportunities with an inflation hedge in all the types of assets mentioned above.

For example, in an industrial property in a highly desirable region, there may be contractual clauses for rent escalations indexed to inflation, with a multinational company as the main tenant. This may make that asset safer for investment than a hotel geared toward the corporate audience in a tertiary market. In this case, however much hotels can adjust their revenues daily, in the current market moment, a revenue adjusted annually with a high degree of reliability may be preferable to hotel nightly rates that may even have to be reduced to attract demand.

Thus, it is essential to always understand, beyond the ability to pass on prices on the supply side, whether there is enduring demand for such assets, something that varies case by case. One of the problems brought by economic instability is precisely that some consumers may reduce their use of a given good or service or simply fail to honor their commitments.

Conclusion

The conclusion is that, in times of high global inflation, more mature economies — where the commitment to price stability is stronger — tend to behave better than more fragile economies, which tend to have less austere governments.

Another important point is that, although rising interest rates negatively impact asset prices in general, some classes suffer more than others. In this regard, real estate assets tend to suffer less than other classes, owing to their ability to adjust rents at a pace similar to the rise in economy-wide prices.

Finally, it is essential that the investor conduct a careful analysis, seeking to understand all aspects of each asset, especially its ability to act as an inflation hedge. In moments of greater uncertainty, it becomes even more relevant to carry out deep due diligence on each investment, taking into account all its particularities.