An article created in partnership:

Over the past decade, the advance of the domestic capital market has been notable. The number of investors on the B3 exchange, for example, grew from 583,000 in 2011 to around 4.4 million in 2022. This movement, largely driven by players such as XP, has intensified competition among players and expanded the range of investment options.

In a more digitalized world, integrated by technology, a natural evolution along this path is the breaking down of national borders and the pursuit of access to the economies and capital markets of other countries as well.

Thus, gradually, more and more investors realize that having 100% of their wealth concentrated in Brazil and denominated in reais is not exactly good diversification, whether due to the small size of the Brazilian economy or to local political and economic instability. In this movement, investors concerned with wealth preservation tend, for the most part, to seek investment options in mature, safe markets with strong currencies, such as the United States and Europe.

However, once the investor overcomes the barrier of the local market and moves into the foreign market, one of the first observations is that, abroad, fixed income offers very low and even negative returns in real terms. At this point, the investor faces a question: how can you invest in mature markets without being exposed to stock-market volatility, while still earning attractive real returns?

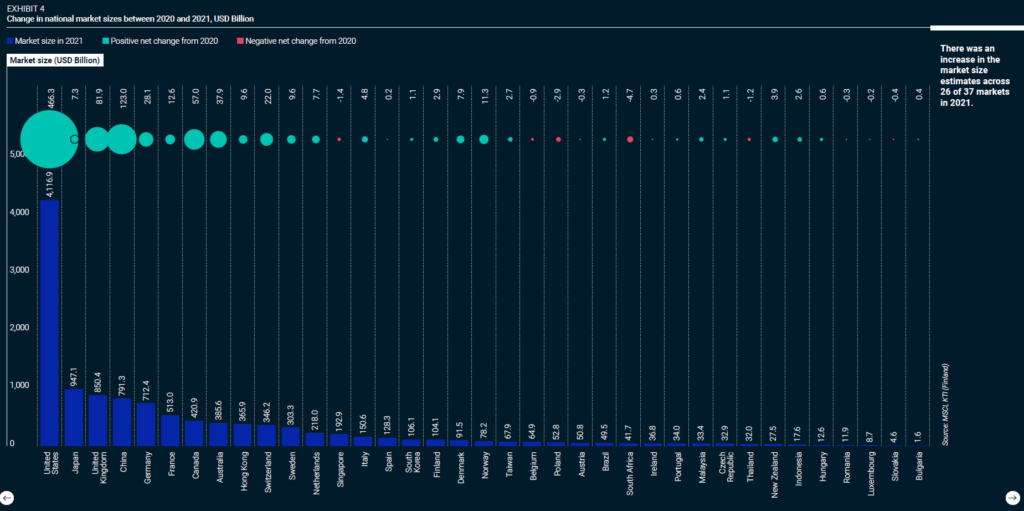

One of the options, quite popular in the U.S., is real estate investment. To give an idea, according to a report by MSCI, a well-known financial information consultancy, the U.S. reached US$ 4.1 trillion in professionally managed real estate investments. Brazil, for comparison, appears with US$ 49.5 billion, equivalent to 1.2% of the size of the American market.

Within the universe of real estate assets, the one best known to the beginning investor is investment in REITs (Real Estate Investment Trusts), very similar to FIIs in Brazil. The issue is that REITs, like FIIs, also suffer from speculative movements and exhibit some volatility in their unit value, which may be undesirable for those seeking wealth preservation.

Another, far lesser-known option is Private Real Estate Investment in the U.S., or Private Equity Real Estate (PERE), a specialty of Ativore Asset, whose main characteristics are described below.

Private real estate investment in the U.S. (Private equity real estate, or PERE)

In private real estate investment, the investor acquires shares of a company that owns one or more properties, as a Limited Partner (LP, with no responsibility for management), while a specialized General Partner (GP) manages the business. If the asset is operational, rents are distributed periodically (generally quarterly) while the GP works to appreciate the property, whether through renovations, operational improvements or tenant turnover.

Another important characteristic of this market is that there is the possibility of negotiation between LPs and GPs, which does not happen in public markets. The negotiation may involve fee reductions, veto rights on acquisitions and sales, early-sale rights, preferred distributions, and so on. These negotiations are usually linked to the amounts invested, to a seed-money contribution or to the formation of long-term partnerships.

In PERE investment, it is also common for acquisitions to be leveraged between 50% and 80%, depending on the asset and the market moment, which helps to leverage returns.

The main advantages and disadvantages of this type of investment, as well as the expected returns, are presented below:

Advantages of investing in Private equity real estate

Low volatility: because they are private investments, not traded on an exchange, they are not directly affected by speculative movements, shifts in market sentiment, capital flows between asset classes or the constant repricing of assets with each new piece of information.

Diversification: because they have low correlation with stocks and fixed-income securities, PERE investment offers good diversification capacity for a portfolio. The same does not hold as strongly for real estate investment in public markets (REITs), since these tend to correlate more strongly with the stock market.

Tangible assets: real estate investment bases its value on a tangible good, widely tradable and considered a good store of value, if well located.

Inflation Hedge: because they are real assets that provide a perennial service (e.g., housing), both rents and asset values have historically tended to be adjusted periodically. In addition, in the U.S. and in various parts of the developed world, residential rent adjustments have persistently outpaced inflation.

Tax benefits: American tax regulation is quite favorable to private real estate investment. Treated as a business, some of the possible tax benefits are the use of depreciation to reduce the taxable base, the deferral of capital gains in the case of reinvestment, and the non-payment of capital gains in the case of inheritance.

Cash flow and appreciation: it is common for PERE investment to return capital periodically (normally each quarter), from rents received, and also upon the sale of the property, when the investor pockets the principal plus capital gains.

Use of leverage on attractive terms to increase returns: in the U.S., the use of cheap credit in PERE investments is very common. This is possible because the property being invested in serves as collateral for the financing, removing much of the risk for the lender. Normally, this is not possible in public-market investment.

“Hands-off” investment: as a limited partner, one can participate in this market with no responsibility for managing the asset, which is handled by the General Partner, in exchange for a management fee.

More imperfect markets: this factor is both an advantage and a disadvantage. The advantage is that it is indeed possible to more easily find mispriced investment opportunities, with favorable risk-return profiles.

Disadvantages:

Low liquidity: being a private investment, there are no organized secondary markets for the assets, which generally go through investment cycles of three to seven years between acquisition and sale. During this period, exit opportunities are more limited.

More imperfect markets: these are markets where there is less transparency and where price discovery is more complex and costly. However, unlike in Brazil, there is plenty of public and private information available, which allows for well-founded decisions. Thus, in PERE investment, knowledge, information, experience, scale, among other factors, tend to disproportionately benefit professional investors and managers.

High minimum investment: these are normally investments aimed at institutional investors or high-income investors. The minimum investment is usually US$ 50,000 to US$ 100,000, which practically rules out entry by the small investor.

Expected returns in Private equity real estate

Quantifying the risk-return profile of private-market real estate assets is no easy task. There are studies indicating that it is better than in public markets and better than in stocks. However, all studies have some kind of limitation, since this is a quite diverse asset class and, as mentioned earlier, with more imperfect markets.

The investor can invest, for example, in the equity or the debt of the property; in more conservative strategies (Core) or riskier ones (Opportunistic); can invest in operational assets or in real estate development. The investor can invest in primary markets, such as New York, or tertiary markets, such as Huntsville, Alabama. Finally, the investor can invest in the most diverse real estate segments – from the traditional residential, offices, hotels, and so on, to cell towers, cold storage and marinas.

Rather than arguing about which asset class has the best risk-return profile, and taking the decision to invest in real estate as given for the diversification this class brings to the portfolio, we leave here only a few return references:

- Private Real Estate Debt (Private Debt Real Estate): IRR of 6% to 12%, depending on the seniority of the debt and the level of leverage.

- Private Equity Real Estate – Operational

- Core strategy, safer segment (e.g., residential): IRR of 10% to 15%

- Opportunistic strategy, riskier segment (e.g., hotel): IRR of 12% to 18%

- Private Equity Real Estate – Real Estate Development

- Safer segment (e.g., residential): IRR of 18% to 25%

It is worth remembering that these figures are merely references and that, obviously, the result is extremely dependent on the quality of the asset, the execution of the business plan and the manager's capability.