In 2021, alternative real estate investments gained more and more ground, reminding investors of the historical resilience of U.S. real estate assets across different economic cycles.

While on one hand the real estate segments linked to the logistics sectors benefited from the sector development brought about by the pandemic, others—such as the hotel sector—deserve special attention given the obvious impacts suffered from the health restrictions arising from the pandemic and the many uncertainties about when travel would be allowed again. Thus, interesting investment opportunities begin to emerge for those with deeper knowledge about the U.S. hotel sector and its nuances.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” Benjamin Graham

Recovery of the U.S. hotel sector

During the period of greatest health crisis, in 2020, government assistance allowed U.S. hotels to withstand the drastic reduction in occupancy levels and, in some cases, to appreciate, through an increase in Net Operating Income (NOI) stemming from a decrease in expenses. In all the hotels in Ativore's portfolio, the government loans received from the Paycheck Protection Program (PPP)—used to cover various costs of adapting to the pandemic restrictions and to reduce the impact of low occupancy during 2020—were 100% forgiven.

The U.S. hotel sector data released throughout 2021 demonstrate a clear recovery of the sector, which is approaching 2019 levels, with occupancy having increased in 21 of the last 33 weeks, through mid-November, as can be seen in the chart below.

Chart 1 - Weekly occupancy, 2019 = 100

Strong weekend demand, which reached 2019 levels, is evidence that leisure travel drove the recovery. Weekday demand is still below 2019 levels, but has been improving since September, a sign that business travel is returning.

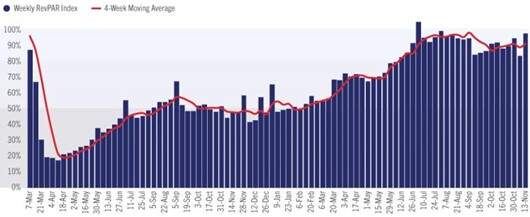

Average daily rates (ADR) in the U.S. have also exceeded expectations. Accounting for inflation, hotel rates were slightly below 2019 levels, except in July, when they surpassed 2019. As a result, in November, revenue per available room (RevPAR) reached its best comparison to 2019 since August, reaching 99% of the level of the same week in 2019, as shown below.

Chart 2 - Weekly RevPAR, 2019 = 100

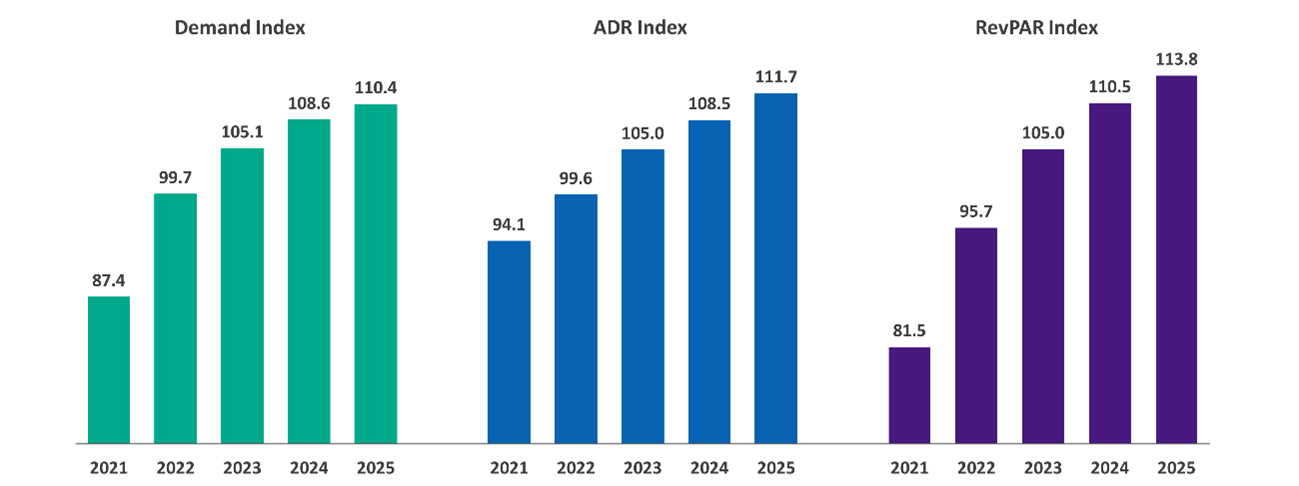

In this way, it is projected that by mid-2023 the metrics achieved in 2019 will already be surpassed, in terms of occupancy (Demand) and average daily rate (ADR) as well as revenue per available room (RevPAR), as can be seen below.

Chart 3 - Hotel sector recovery forecast, 2019 = 100

Opportunity in distressed alternative investments in the U.S.

The moment of economic recovery the U.S. is experiencing favors opportunistic acquisitions in sectors most affected by the pandemic, such as the hotel sector.

We have several leisure hotels in the U.S. in our portfolio, for example, that already have operational results in line with or better than those of 2019, but given the market moment with strong fear among traditional investors—and because they are alternative investments—still at prices below pre-pandemic levels. Meanwhile, real estate segments such as residential and logistics, which performed better during 2020, are at prices equal to or higher than 2019 and already show lower yields than pre-pandemic, depending on the leverage structures adopted.

In a macroeconomic context of rising inflation, investment in hotels with resilient fundamentals proves interesting, as this is the class that is able to respond to inflation most quickly, with the ability to adjust the rental rate daily—unlike, for example, contracts for logistics warehouses with large companies, in which rent is usually adjusted annually, at best.

The hotel sector has two major segments: leisure hotels and business hotels, and both were greatly harmed by the pandemic, as they were forced to close for much of the time. However, in the U.S., where the economic recovery is more advanced than in Brazil, leisure hotels already have occupancy at levels equal to or higher than in 2019, due to very strong pent-up demand. Business-oriented hotels, on the other hand, are still at a greater level of uncertainty, since it is unclear when and whether corporate travel will return to pre-Covid levels.

The most important thing in any type of investment in a scenario of rising inflation is having the ability to pass costs on to the consumer, and in the case of hotels, this is a great advantage—also depending on the type of traveler staying there. For example, if an executive has to choose between taking a routine business trip, which is increasingly being deprioritized vis-à-vis online meetings, or holding the meeting from their office at no cost, high lodging prices will be a crucial factor in the decision. In leisure hotels, on the other hand, this demand tends to be less volatile, because with the mass resumption of tourism, there is pent-up demand combined with greater household savings, which allows for higher vacation spending and thus an acceptance of this inflationary pass-through.

In short, it seems to us that the current moment—in which leisure hotels are beginning to recover from the pandemic, but in which there is still considerable pessimism on the part of the market regarding this segment—may present rare acquisition opportunities for investors.

There are hotels that suffered foreclosure or needed to sell the asset at any price, due to poor management during the pandemic, generating very low cash flow; and there are also hotels with greater seasonality—such as hotels near ski resorts—that have not yet enjoyed the high season (winter, from December to March) since 2019 and need additional capital to remain operational.

The importance of being specialized in alternative investments

The U.S. hotel sector can be quite profitable for investors and tends to generate quite high cash flows (often above 10% per year in dollars). However, as with any investment, it is important to have the advisory support of professional investors specialized in this segment, because there are several nuances related to the acquisition value, the hotel's specific segment, positioning, flag, location and management processes that have a fundamental impact on the profitability of this type of investment.

Get in touch with one of our advisors to learn more about the investment opportunities emerging in the U.S. hotel sector in this post-pandemic moment.

“Risk comes from not knowing what you are doing.” Warren Buffett

Paulo Camargo

- Origination and product-monitoring analyst and associate at Ativore, an economist from UFRJ, with part of his studies completed at King's College London.

- Responsible for prospecting new investment opportunities for capital allocation and monitoring the products in the portfolio.

- Previously, he worked in the treasury of Grupo Trigo and in the credit recovery area of Saphyr Shopping Centers, both leading holding companies in their respective fields.