While Brazil is experiencing moments of political and economic tension, with successive interest rate hikes, rising inflation and a depreciating Real, in the U.S. the economic recovery continues at a fast pace. With 2022 being a presidential election year here, there is no sign of a truce for the local investor. In this environment, investing abroad makes more sense than ever.

Despite its profound economic and social impacts, the pandemic also brought several real estate investment opportunities in the U.S. On one hand, some more directly affected segments—office buildings, strip malls, senior living and hotels—saw their prices remain stable or even pull back slightly over the past 12 months. On the other hand, the low cost of real estate financing—reaching less than 3% per year—with the sharp drop in interest rates, increased the gains from project leverage. Strong demand for capital, in turn, also caused the private credit market to expand strongly, with stable gains above 10% per year.

Opportunities for investing abroad in certain U.S. real estate segments

Warren Buffett: “Be fearful when others are greedy.

Be greedy when others are fearful.”

The current market moment, one of economic recovery, has favored opportunistic acquisitions in the segments most affected by the pandemic. Several leisure hotels in the U.S., for example, already have operational results in line with or better than those of 2019, pre-pandemic.

Another example is office buildings. Although no one knows for certain what the dominant pattern of use of these spaces will be going forward (in-person, remote or hybrid), the fear surrounding the segment has caused the drop in prices to more than offset any eventual drop in occupancy. At Ativore, for example, we have analyzed office buildings with discounts of up to 75% relative to construction cost and that need less than 50% occupancy to reach their economic-financial break-even point—which can be an excellent opportunity, depending on the project's business plan.

We have also analyzed many Senior Living properties at discounted prices. The wariness of some investors, given that it involves a more vulnerable population, has generated interesting opportunities in the segment, which has not yet fully recovered but will eventually return to normal operating levels, especially considering the aging trend of the population.

Street retail, represented in the U.S. by Strip Malls, has also experienced a resumption in activity. Well-positioned assets, with healthy anchor stores and supermarkets, have paid annual dividends of 9% to 11% with IRRs around 14%.

Another lesser-known segment, but one that has also been a great option for more defensive portfolios, is Private Real Estate Credit, in which the investor, participating in a pool, grants loans to real estate projects, obtaining fixed returns around 10% with the property as collateral.

Opportunities for investing abroad generated by the low cost of financing

Another facet of the pandemic was the injection of capital into the economy and the maintenance of interest rates at historically low levels. This movement has also generated quite interesting acquisition opportunities.

At Ativore, for example, we have seen fixed interest rates as low as 2.8% per year for assets considered safe. And even in segments more affected by the pandemic, such as office buildings, it is not uncommon to see rates below 4.0% per year, fixed for 5 years or more.

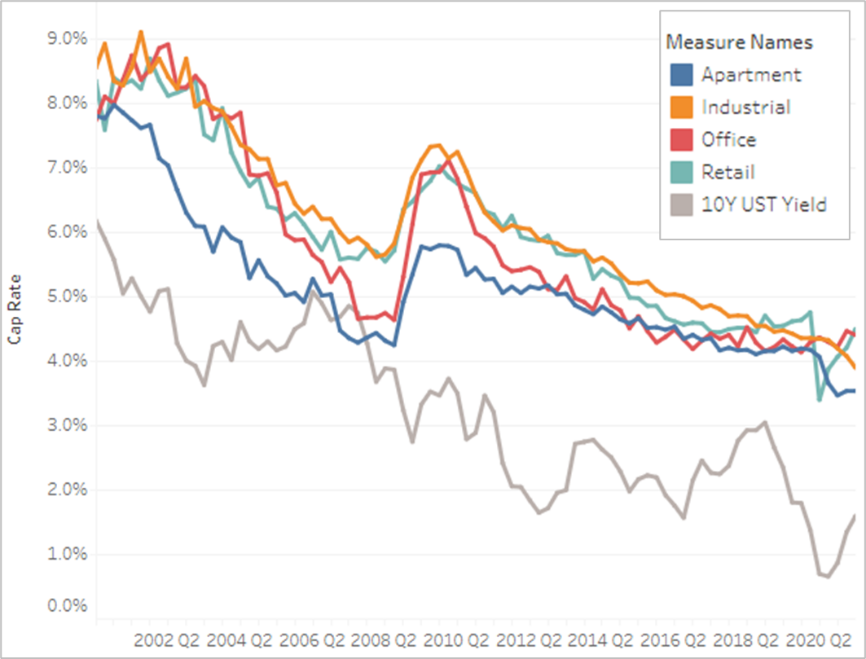

The uniqueness of the current moment comes from the fact that the gain generated by cheaper financing has more than offset the increase in property prices. Normally, the drop in the base interest rate tends to be accompanied by an increase in asset values, which is represented by the reduction in property capitalization rates (cap rates). However, what was seen in several segments was an increase in the spread between the base interest rate and average cap rates.

In the first chart, the spread is represented by the difference between the gray line, relating to the base rate for a 10-year U.S. government bond, and the colored lines, referring to the cap rate in each market segment—apartments, industrial, offices and retail.

Chart 1 - NCREIF Capitalization Rate by Property Type and 10Y UST Yield

Source: NCREIF, Board of Governors of the US Federal Reserve System via FRED, Milionacres, September 2021

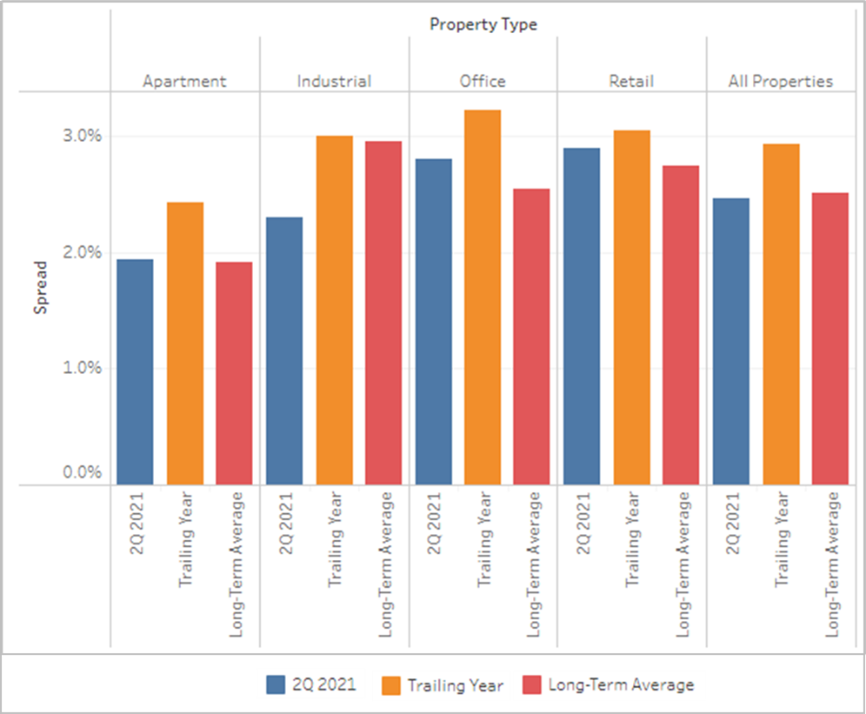

In the second chart, it can be observed that, in all segments, the current spread (orange bar) is larger than the long-term historical spread (red bar).

Chart 2 - Capitalization Rate Spread by Property

Source: NCREIF, Board of Governors of the US Federal Reserve System via FRED, Milionacres, September 2021

On one hand, a larger spread signifies a higher perception of risk in the segment compared to the historical average. On the other hand, it means that properties, in general, can be acquired with extremely attractive financing relative to their current prices, which leverages investors' gains.

Conclusion

Obviously, each real estate asset is unique and its particular characteristics can easily override the market cycle, both positively and negatively. In this sense, there are opportunities in all segments, even in residential or industrial, which are experiencing a heated moment. With interest rates so low and with some market apprehension regarding certain segments, it is possible to obtain quite interesting returns from opportunistic acquisitions. The most important thing, however, is that a careful analysis of each asset be carried out.

Finally, given the political and economic context in Brazil, the forecast that we will have more volatility in 2022 and the historic window of opportunities in the U.S., the moment to internationalize part of one's investments could not be more opportune.

*Point your phone camera or click on the image to talk to a partner advisor