The rise in interest rates in the United States is once again in the crosshairs of market analysts, leading to concerns about its eventual impact on the U.S. economy.

Regardless of the moment, it is necessary to consider all relevant factors when examining the U.S. economy, always seeking more than one source. Here, the old saying applies: trust, but verify.

When observing the U.S. economy, some factors are highly relevant:

- The Consumer Confidence Index for August 2018 was one of the highest in the last 18 years, almost as high as that of August 2000¹;

- Wage growth in June 2018 was 2.9%, the highest since 2008²;

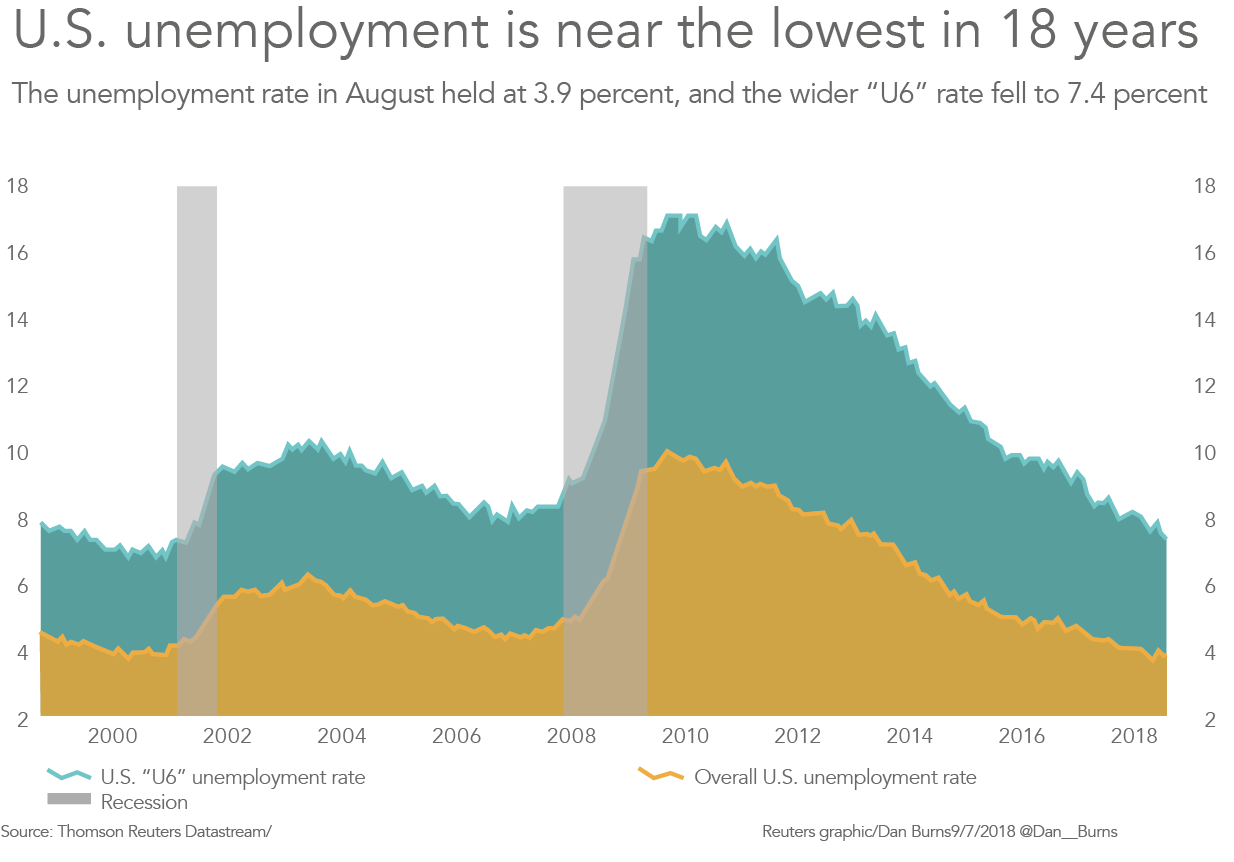

- The current U.S. unemployment rate is the lowest since 2001. Also considering the wage growth in August 2018, the annual increase in per capita income was the sharpest since 2009³.

A survey conducted in May of this year by the National Federation of Independent Business brought three significant conclusions: the forecasts for economic expansion are the most optimistic of all time, corporate profits are at their highest level since 1995, and the outlook for rising goods prices is the highest since 2008.

With all this growth in the U.S. economy, the increase in interest rates is something healthy to achieve a monetary counterbalance and avoid economic overheating, since you do not want to create a fictitious economy that grows based on low interest rates. However, it is important to assess in detail what will happen to multifamily income properties in this scenario. In other words, will residential buildings sustain the generation of operating revenue from the first month? What are the opportunities and risks in multifamily income investments in an economy with higher interest rates?

To address the points above, it is first necessary to understand the demographic trends between baby boomers (the generation born between 1946 and 1964) and millennials (from 1981 to 1997), and the current state of the U.S. real estate market.

Millennials are the largest generation in U.S. history, with more than 75 million individuals, and they have particular behavioral characteristics relative to previous generations. They are less inclined to own a home, prefer a greater degree of mobility (moving to other cities or finding new jobs) and are taking longer to marry and have children. Combined with this, student loan debt has reached US$ 1.5 trillion, the highest value in history, indicating this generation's high level of indebtedness.

They do not have a saver's profile and, therefore, do not usually have the amount needed for a down payment to buy a property, which is aggravated by the fact that there are fewer and fewer cheap (affordable) homes to buy. For these and other reasons, millennials prefer to rent rather than buy their own home.

The situation of baby boomers is different. They have an inelastic income (one that does not keep up with the cost of living), health-related expenses grow constantly, they are among the demographic generations with the highest bankruptcy rate (a 204% increase from 1991 to 2016)4 and, currently, 42% of them have no money saved at all5.

Something important to highlight is that an increase of just 0.25% in the interest rate reduces the ability to buy a home by 3%. In other words, if interest rates rose by 1%, the buyer would have to reduce the financing by 12%, having to put down a larger down payment to buy the same property. This is one more point that makes renting the best option for many people at this time6.

Another interesting factor: according to a survey conducted by the Federal Home Loan Mortgage Corporation (Freddie Mac), 78% of Americans believe that renting is a more economical option than buying their own home, and the percentage of people who say they do not want to buy a house has also increased.

Another survey, by the National Apartment Association (NAA) in the U.S., reports that there is demand for 4.6 million apartments by 2030, just to meet projected demand7.

However, the great dilemma is that new properties are becoming increasingly expensive, because the costs of building materials, land and labor are high. Additionally, many cities are reviewing their building codes to have more control over what they allow to be built, something that also increases the final cost of housing. Such factors culminate in a crisis generated by the lack of affordable housing for the population, whether houses or apartments in the U.S.8.

With all these factors presented, and despite rising interest rates, demand for housing remains very strong and tends to grow. However, the cost of that housing will increasingly be the central issue in the decisions to be made.

So, what will happen to multifamily income properties? Will it still be possible to find them? Yes, they will always be available and demand for them will also increase. It is up to specialized companies to develop processes to find the best properties.

At CONTI Real Estate Investments, we acquire properties financed with fixed 10-year interest rates, even amid market changes. The most important thing for the investor is to check the culture of the company specialized in acquiring and managing this type of property. How do they interpret opportunities and risks? What are their processes and goals? What is their business track record? How are daily activities executed?

On this point, Peter Drucker, the great guru of business management, put it well: “Culture eats strategy for breakfast.”

*Carlos Vaz is founding partner of CONTI Real Estate Investments

References

1The Conference Board

2Federal Reserve Bank of St. Louis

3Reuters

4Consumer Bankruptcy Project

5Federal Reserve's Survey of Consumer Finances

6Magnify Money, using data sourced from Federal Reserve

7National Apartment Association

8The Wall Street Journal, March 2018 - The Next Housing Crisis: A Historic Shortage of New Homes