COVID-19 is the first pandemic we have faced in modern times, and the level of uncertainty about its impact on the U.S. economy remains very high. However, regardless of whether this recession is V-shaped, U-shaped, or W-shaped, what we know for certain is that a large number of owners will be late on or will default on their loans.

There is no doubt that this is a challenging environment for investors, especially for those exposed to the hardest-hit sectors. Yet this disruption should generate unprecedented opportunities to invest in the U.S. real estate market.

The resilience of U.S. real estate portfolios to the crisis

Following the bloodbath seen in global financial markets, it is now possible to begin to see more clearly the impact of the lockdown on the real estate sector. According to the most recent projections from the Urban Land Institute, the RCA property price index is expected to fall 7% in 2020, rise 1% in 2021, and rise 5% in 2022. This is a broad index, and property price behavior is highly specific to both location and segment.

Specifically, the real estate private equity portfolios of Ativore's clients have proven surprisingly resilient, with occupancy and rent-collection levels above initial projections, with variations across the following market segments:

- Self-storage, medical office buildings, office buildings, industrial properties, and private debt felt little or no impact on occupancy levels and tenant delinquency.

- The impact was smaller than expected in the case of single-family and multifamily homes, and senior living, with a slight increase in vacancy and delinquency (a 5% to 10% reduction in revenue).

- Strip malls and hotels suffered a substantial impact, in some cases exceeding 80%. However, due to the strong reserve levels of these properties, appropriate leverage, and the management actions taken by operators, which included substantial cost cuts and access to U.S. government emergency programs, no long-term capital losses are anticipated.

The case for opportunistic investments in U.S. real estate

Highly leveraged owners or those with limited reserves will need funds to weather the recession, and many will be forced into distressed sales at heavy losses. At the same time, a unique combination of additional factors strengthens the case for opportunistic acquisitions over the coming months:

- Mortgage financing rates in the U.S. are at historically low levels, providing an almost unprecedented opportunity to increase rental yields through leveraging acquisitions at very low costs.

- At some point after the crisis, the reductions in interest rates will be reflected in higher property values, due to the compression in their respective capitalization rates (cap rates).

- There is very strong pent-up demand for several asset classes (chiefly multifamily and self-storage properties), and the pandemic has halted practically all construction projects, indicating strong appreciation potential from insufficient supply once the market returns to normal operation.

- There is extensive documentation of a global trend toward increasing capital allocations to real estate as a way to avoid the volatility of financial assets. This is the so-called "flight to safety" of the real estate sector, which continues to offer the best risk-adjusted returns.

- The magnitude of the rescue package already approved in the U.S. (20 times larger than the Marshall Plan in present-day terms) should lead the U.S. economy to emerge ahead of other economies, attracting global capital to U.S. real estate.

The positioning of global real estate investors

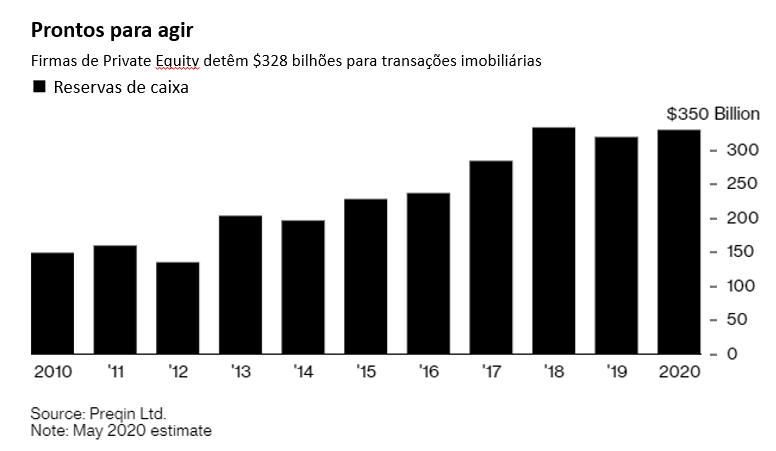

The world's largest real estate investors, including Blackstone Group, Brookfield Asset Management, JP Morgan, and Goldman Sachs, among other institutions, are holding high cash reserves and raising substantial capital for the opportunities created by the pandemic, with a focus on real estate.

This type of opportunity takes some time to appear in a recession, but these firms are already beginning to identify some distressed properties as potential acquisition targets.

According to Alisa Mall, Director of Investments at the Carnegie Corporation, a New York-based foundation, the current moment of unprecedented uncertainty favors investment strategies in multi-sector real estate funds that offer the flexibility to take advantage of differentiated market opportunities and conditions by real estate segment and geography.

Ativore's strategy for resuming investments

Identifying good acquisition opportunities during a recession requires experience in pricing real estate in times of stress and is safer when done through co-investment with local operators specialized in acquiring distressed operational (cash-generating) properties for the subsequent implementation of improvement actions. It is a medium- and long-term strategy, as it is necessary to work on stabilizing the properties and holding them until the economy recovers.

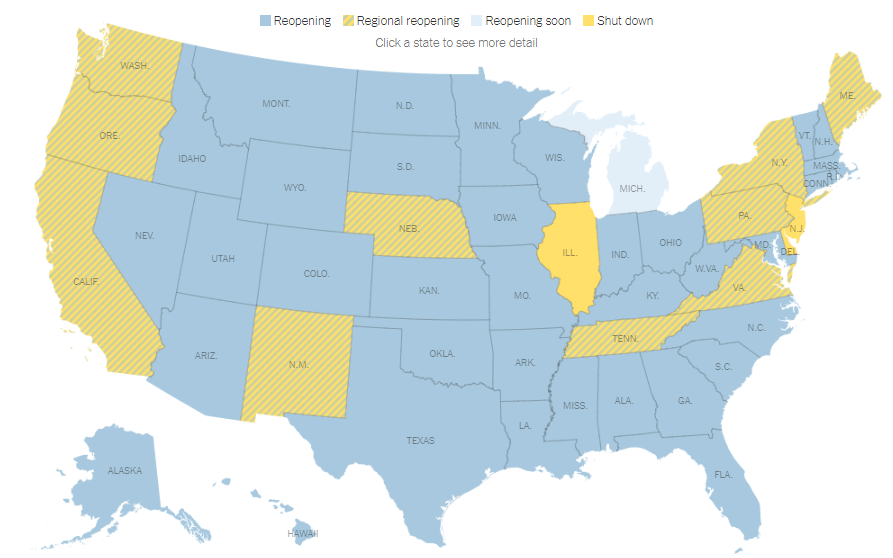

Most U.S. states have already been implementing a phased plan to reopen their economies, as reflected in the map below:

Although we estimate that normalcy will only return early next year, many owners will not be able to survive this period. Larger discounts on distressed assets should begin to appear once the forbearance periods under the CARES Act begin to expire, in July and August (90 days), and we will begin to look at possible opportunistic acquisitions from those dates onward.

There is a trade-off between the level of uncertainty and the size of the opportunities that will emerge. If we wait too long for the situation to become sufficiently clear, we may have missed the best opportunities, and if we enter too early we run the risk of seeing our assets lose value over the short and medium term before recovering.

Several of Ativore's partners in the U.S. have already begun to identify distressed properties at substantial discounts to the market, and our product team is watching these opportunities closely. We will be selective in our investment decisions and will target return goals above 15% per year, including rent and appreciation.

We will prioritize co-investment with real estate sponsors with extensive experience in already operational (income-generating) properties, in segments that have shown greater resilience to the crisis, such as self-storage, medical office buildings, industrial properties, single-family and multifamily homes, and senior living, in order to minimize risk in a time of uncertainty.

We will carefully analyze opportunistic investments in distressed properties in sectors such as retail and hotels (with discounts above 30%) for small allocations, as a way to enhance the return of clients' portfolios over the medium and long term.

Diversified portfolios, in which we have the flexibility to take advantage of market conditions across various asset classes, may be more attractive in this time of uncertainty than single-sector strategies. It will be asymmetric. Different sectors and geographies will give rise to distinct opportunities, and there will be no uniform recovery. It is important to look at each individual opportunity and determine whether there is a critical success factor for the transaction, regardless of the asset's sector.

Feel free to get in touch with us to explore the issues discussed in this article in more depth.

Learn how to invest in income-focused real estate portfolios in the U.S.