The current economic environment in the U.S. and around the world is being viewed with considerable apprehension. Markets are still uneasy about the persistence of high inflation and the Fed's repeated interest rate hikes to try to contain this effect. This creates a negative climate of distrust, especially in the news, with growing fear of a possible recession.

However, the long-term investor, especially in the U.S. real estate market, should maintain a certain distance so as not to be infected by the alarmism – characteristic of short-term investors – that frequently is not supported by the data. More than that, the long-term investor can even take advantage of moments of short-term volatility to access good investment opportunities.

Origins of short-term volatility

The challenges recently faced by the U.S. economy are a direct consequence of the pandemic. As we know, a little more than two years ago, the onset of the pandemic tormented the country, with the closure of many establishments due to health measures. This caused mass layoffs, with more than 20 million Americans losing their jobs in the first months of lockdown. In an attempt to contain the economic disaster that was to come, the Fed carried out a series of fiscal stimulus measures, such as loans and monetary aid packages, injecting nearly 3 trillion dollars into the economy.

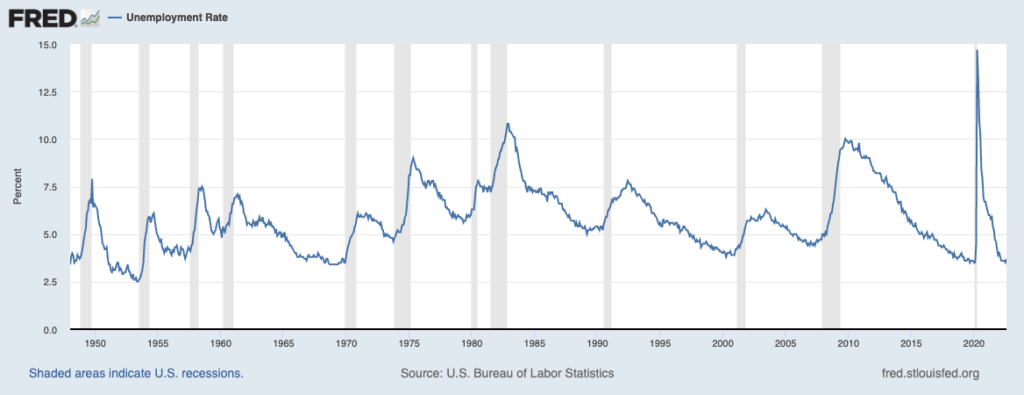

Two years later, after the mass vaccination of the population and the subsequent lifting of mobility restrictions, the economy returned to full operation, recovering, in July 2022, all the jobs eliminated during the isolation period, as can be seen in the chart below.

However, the Covid-19 outbreak brought other challenges to the country's labor market: driven by the early retirement of Americans nearing the end of their careers, the reduction in immigration and the abandonment of jobs by workers who began caring for close relatives, the labor available in the country fell considerably. This phenomenon created a jobs imbalance, with more opportunities being created than there were unemployed people. As a result, companies had to compete for workers, causing a 5.5% increase in the country's average wage compared to the previous year (double the average rate of recent years), contributing to the rise in consumption in the country and, consequently, to high inflation. Thus, despite the climate of uncertainty, the labor market remains robust and the unemployment rate, in August, remains low, at 3.5%, the same level as in February 2020, already historically low.

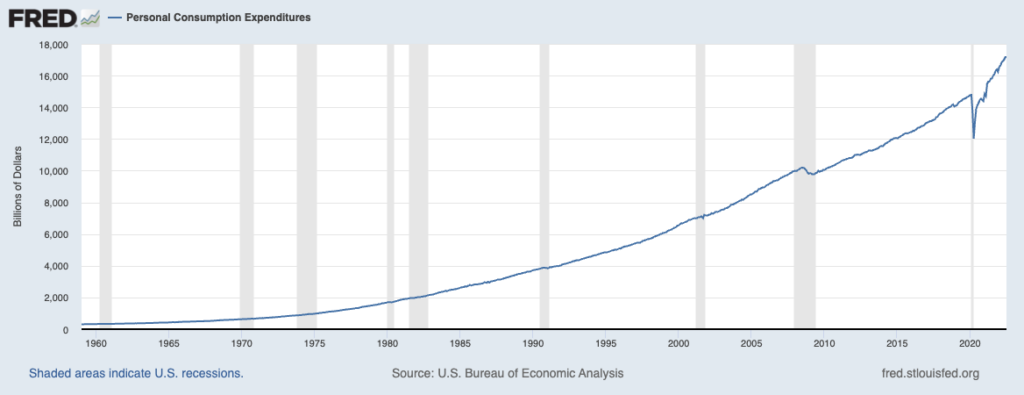

Personal spending also remains at historically high levels, partly a result not only of rising prices and the injection of government money, but also of the record level of savings accumulated in the U.S. during the most acute months of the pandemic.

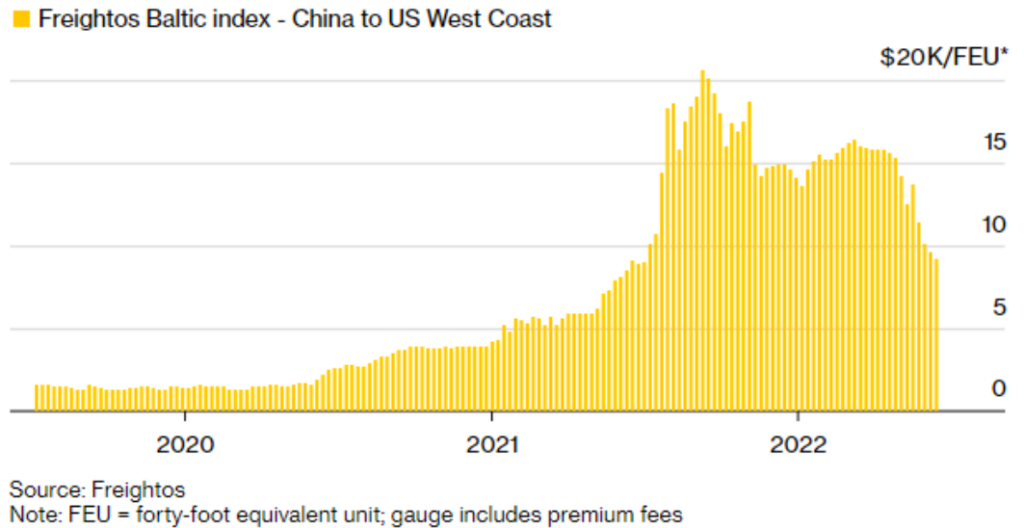

Another point that contributed and still contributes to U.S. inflation was the closure of some Chinese ports, especially the port of Shanghai. This movement caused an increase of about 10 times in the cost of transporting cargo from Asia, as well as an increase in the average transport time, affecting global logistics chains. This directly impacts U.S. production costs, pressuring inflation. However, this is an effect that is beginning to show signs of fading and that certainly will not persist in the long term.

The intention here is not to downplay the importance of record global inflation, nor to dismiss global economic fragilities. However, it is necessary to put things in perspective and distinguish what is short-term volatility from what is a long-term trend. Thus, even with the problems of inflation and rising interest rates, other economic factors are positive and the market consensus still projects that U.S. GDP will grow 1.6% in 2022.

In the real estate market, where short-term volatility tends to be less important, the investor should make decisions based on long-term trends and strive not to be so strongly influenced by the market's moods. Below, we discuss the outlook for some of the main segments of the real estate market during the pandemic and now, after all restrictions have been lifted.

General overview by real estate segment in the U.S.

Multifamily

Due to the pandemic, many events that drive the formation of new households, such as weddings, company relocations and starting college, were postponed. With mass vaccination, the end of restrictions and the recovery of the economy, this pent-up demand could be met. As a result, the net absorption of residential units was a record in 2021, with a positive net balance of approximately 660,000 occupied units, with the first quarter of 2022 following this trend (110,000 units absorbed in the period).

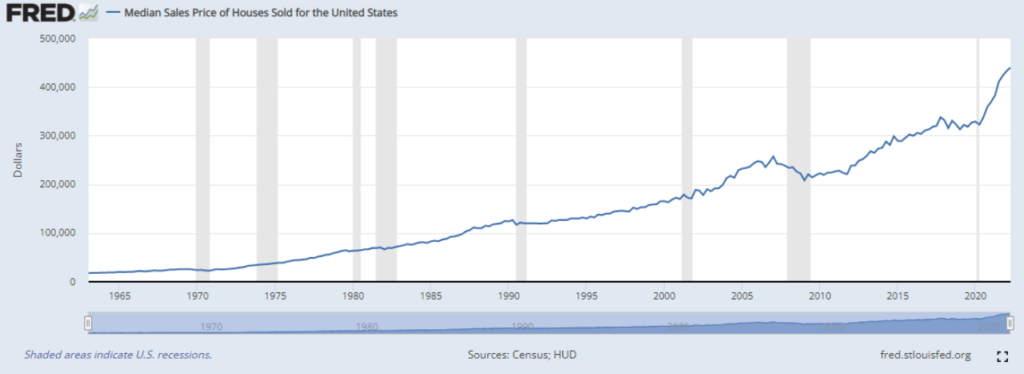

As a result, in the first quarter of this year, the apartment vacancy rate in the country fell to a historic low of 2.4% and rents posted record growth of 17.3% over the last 12 months. It is important to note that, during the pandemic, there was a national moratorium against the eviction of delinquent tenants, and, for this reason, many owners chose to keep rents frozen, offsetting this measure with recent increases. Even so, strong demand drove sale prices of single-family homes up 34% over the last two years, which corroborates the housing-shortage thesis.

Self-storage

The self-storage sector was also influenced by the movement of household formation. At the beginning of the pandemic, properties in this segment reduced the rents they charged in order to maintain occupancy levels. With the increase in the number of households, the moves and remote work (which prompted people to make room in their homes to set up an office), demand for storage units increased.

As a result, vacancy in this segment reached a historic low of 6.6% at the end of 2021, accompanied by 7.6% rent growth since 2020. Demand is expected to cool slightly and more assets of this type are expected to be built. Even so, the projection is for vacancy to rise only slightly to 6.9% by the end of 2022, with rents growing around 4% for the year.

Industrial

Like the residential and self-storage sectors, the industrial asset sector also posted historically positive occupancy figures. The “Covid zero” policy instituted by the Chinese government caused cities and ports to close, directly affecting global supply chains. Struggling to find products manufactured around the world, U.S. companies are seeking warehouses for storing and producing goods within the country, in port regions or distribution hubs (“onshoring strategies”). As a result, demand for assets in this segment has been increasing since the start of the pandemic, reaching a historic low vacancy of 3.9% in 2021 and, despite the projection of a record delivery of 400 million square feet in 2022, vacancies are expected to continue declining this year.

An important point to note is that certain global chains are changing permanently, with a trend toward bringing production lines into the U.S. Examples such as Samsung, which is opening a chip factory in Texas, and Toyota, which is opening an electric-car assembly plant in North Carolina, are becoming more common. Another possibility being pursued is bringing production to Mexico or Canada, which is already reflected in the cargo-transport figures across the borders with these countries.

Retail

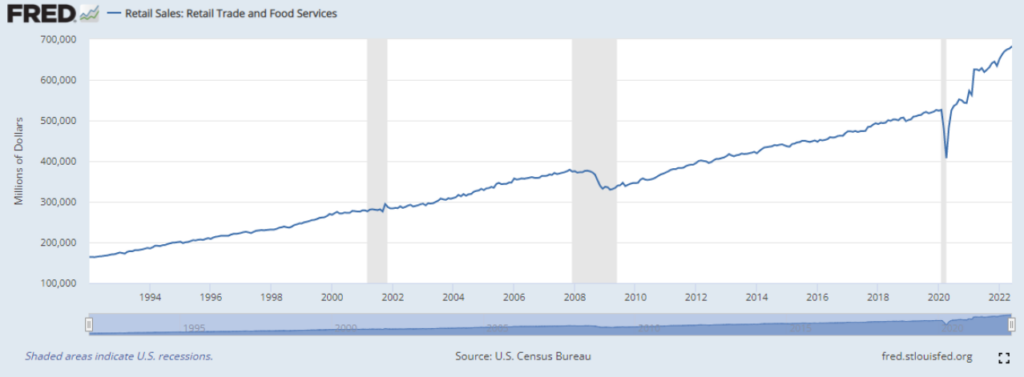

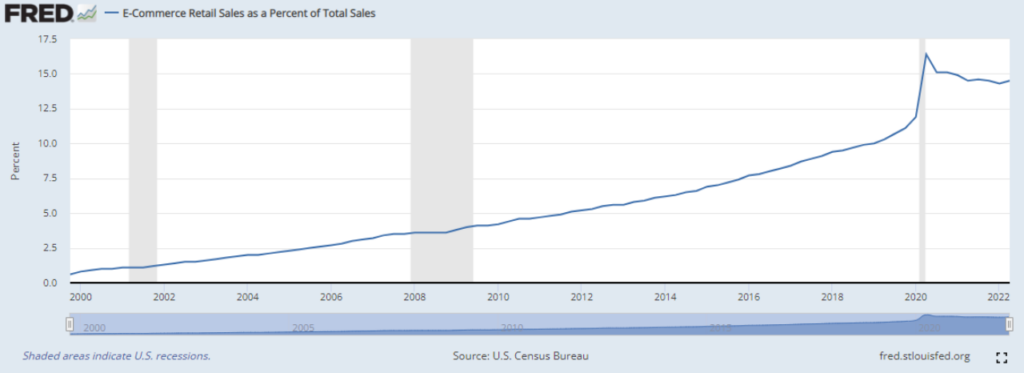

As mentioned earlier, retail sales recovered from the first wave of the pandemic at a very strong pace, reaching a level 30% above that of the isolation period and well above inflation. Despite the belief that consumption is being supported by the growing predominance of e-commerce, the numbers show the opposite: online shopping peaked at the start of the pandemic, representing more than 16% of total consumption, but fell and has remained stable since then, at around 14%. Meanwhile, brick-and-mortar store sales are nearly 20% above the pre-pandemic period.

The vacancy of retail assets with more than one tenant was at 5.7% before the pandemic and rose because of it, reaching 6.8% in mid-2021. However, after the end of the restrictive measures, this rate began to fall again, ending last year at 6.1% and with the projection of ending 2022 below 6.0%.

By analyzing the numbers and observing trends, it is possible to find several investment opportunities that run counter to the speculation about the economy. Not surprisingly, the number of commercial real estate transactions in 2021 also reached a historic record, with nearly 30% more transactions than the previous high, in 2018. The prices of properties such as hotels, offices and retail centers, which were most impacted by the pandemic, rose 13% relative to 2019 values, while apartments, self-storage and industrial properties posted more substantial increases (23%, 35% and 51%, respectively). In addition, it is important to note that real estate investments are well positioned to protect against inflation, having a good ability to adjust rents.

In short, it is undeniable that the U.S. economy is facing some obstacles, particularly high inflation and its consequences, such as rising interest rates. However, part of the problem is precisely caused by the health of the U.S. labor market and economy. In the short term, it is inevitable that there will be corrections in asset prices, which have been heavily inflated by the pandemic stimulus, and that there will indeed be some kind of cooling. In the long term, however – the focus of real estate investments – no structural problem is apparent. It is therefore up to the investor to seek out opportunities and take advantage of the current volatility.