The Park Crescent multifamily is a 400-unit “garden-style” property located in Norfolk, the second-largest city in the state of Virginia. The asset was acquired in 2019, before the pandemic, for US$ 57.2 million and was sold in May 2024 for US$ 84 million, a 47% appreciation, even amid the most adverse market scenario. For investors, considering distributions over the course of the project and the capital gain, net of tax in the state of Virginia, an Internal Rate of Return (IRR) of 15.2% per year and an Equity Multiple of 1.85x were achieved—that is, a total return of US$ 185 thousand for every US$ 100 thousand invested. This is a good example of the resilience of residential real estate investment, especially when management is active and the market of operation is carefully selected.

Below, the strategy adopted and the operational results that made the investment return possible will be discussed in greater detail.

The asset

Park Crescent is a multifamily built in two phases, the first in 1991 and the second in 2012, with 288 units and 112 units in each phase, respectively. One factor that differentiates it from the competition is that the property holds some of the largest units in its market, with an overall average size of 1,137 square feet (105 m²). While the Phase I units have an average size of 1,277 square feet (119 m²), the Phase II units, which are mainly one-bedroom apartments with a kitchen open to the living room, have an average size of 776 square feet (72 m²).

Norfolk has a population of about 230 thousand inhabitants and is considered a tertiary market in the U.S., which does not mean it is not an interesting market for real estate investment—quite the opposite. This classification is much more related to the size of the market and transaction volume than to the quality of the real estate investments themselves. In this case, more important than investing in markets well known to the general public, it is essential to understand the dynamics of each market, its economic fundamentals and the balance between supply and demand for properties.

Business plan

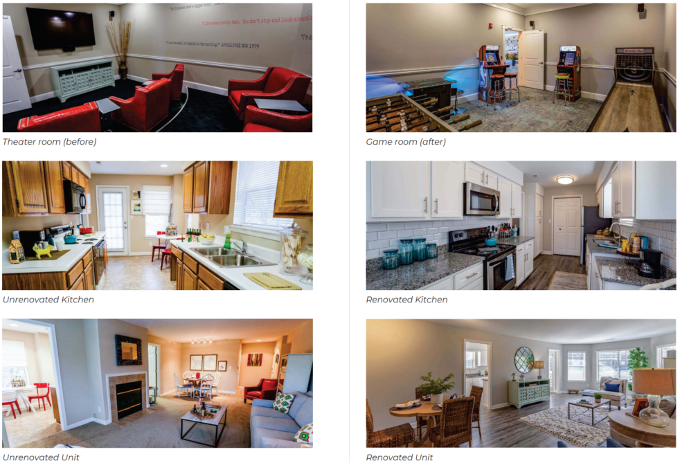

Although the Phase I units were significantly larger than those of Phase II, they had not been renovated since their construction in 1991, which in itself would already be a good opportunity to increase rents after renovations and modernizations.

In this case, the demand for renovated units was evidenced by Park Crescent itself, as the Phase II units achieved average rents of US$ 1.34 per square foot, compared to US$ 0.97 per square foot for Phase I (a 42% premium). The Phase I units had original cabinets and countertops, white appliances, original lighting and carpets. The Phase II units, on the other hand, had higher 9-foot (2.75 m) ceilings, with more modern cabinets, flooring, lighting and appliances.

The business plan, then, consisted of carrying out a classic “Value-Add” strategy – repositioning the property, modernizing the interiors of all units and also improving the common areas and amenities, in order to improve the tenant experience and also make the property more aesthetically attractive. In addition, it consisted of improving its operational performance through management improvements, with increased revenues and reduced costs.

Additionally, a potential upside related to the fact that the property had some elevators out of operation since the acquisition. The preference would be for their full decommissioning, since the most common arrangement in properties of only three floors is not to have elevators. This decommissioning would depend on approval from the city, and would generate resource savings both by eliminating the need for replacement and by reducing maintenance expenses. In any case, should there be a need to replace the elevators, supplementary financing had been arranged so that there would be no need to capitalize the business.

Before-and-after renovation photos

Property performance

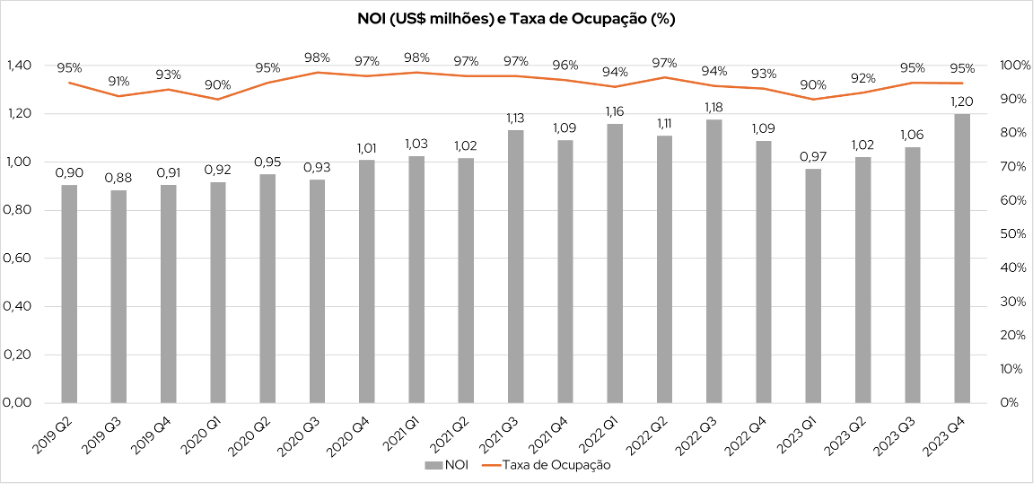

With the planned renovations to the units and common areas, as well as operational improvements, Net Operating Income (NOI) gradually rose from about US$ 900 thousand per quarter to just under US$ 1.2 million per quarter, an increase of approximately 30%, and with relatively stable occupancy, ranging between 90% and 98%, as a function of local dynamics and the seasonality common to residential leasing. In addition, as is common in the Value-Add strategy, part of the vacancy is attributed to the fact that about 20 units (5% of the 400 units) remained under renovation each month for the execution of the strategy.

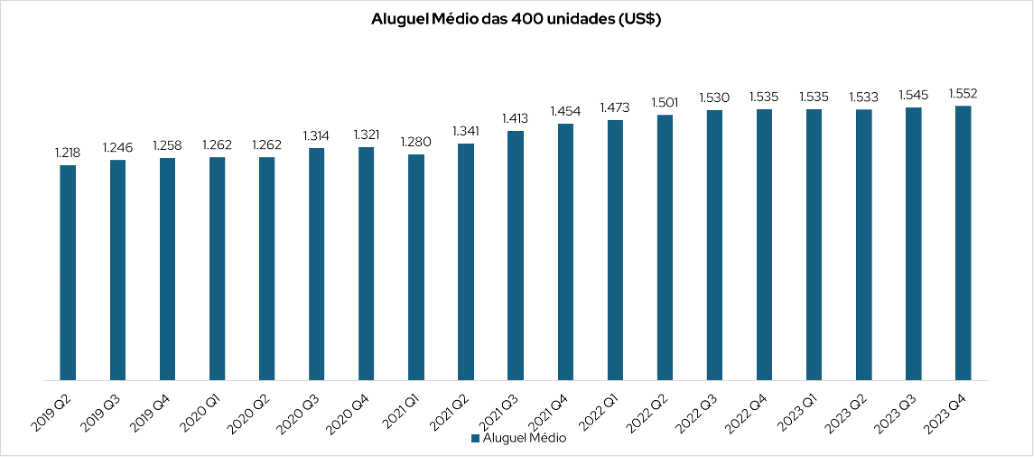

In terms of the average rent of the 400 units, it is possible to see the operational evolution of the property. At acquisition, the average rent stood at US$ 1,218, a figure that gradually rose to the level of US$ 1,530, when the stabilization process began—that is, when all units had already been renovated and growth comes only from local rent inflation and no longer from the premium obtained on the renovated units.

Returns for investors

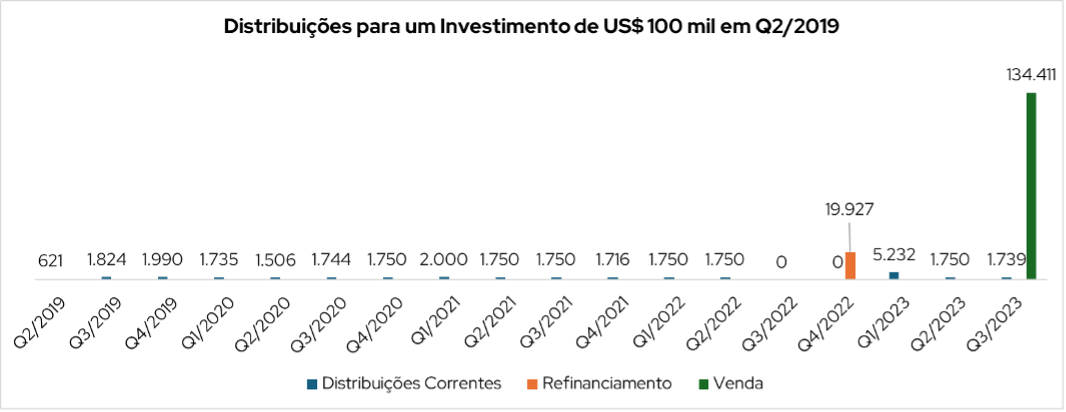

In terms of distributions to investors, even with the operational improvement, a conservative stance was adopted, opting for stability in disbursements, which is also common in this type of strategy. On average, the goal was to make a distribution of around US$ 1,750 per quarter or US$ 7,000 per year for every US$ 100 thousand invested, equivalent to an annual distribution of 7%.

The exception occurred in the third and fourth quarters of 2022, when distributions were withheld, due to the imminent outcome regarding the replacement or decommissioning of the elevators. In parallel with the interruption of distributions, supplementary financing was obtained in case the decommissioning was not authorized.

Finally, with the authorization of the decommissioning, the gains from the refinancing were distributed and an extraordinary distribution was made in the first quarter of 2023, also covering the withheld distributions relating to the two previous quarters.

With these distributions, which are already net of capital gains tax withholding in the state of Virginia, the investment had an IRR (Internal Rate of Return) of 15.2% per year and an Equity Multiple of 1.85 times—that is, in total, US$ 185 thousand was returned for every US$ 100 thousand invested, an excellent performance considering the adverse market moment, with higher interest rates and less liquidity.

Sale timing

With the elevator issue resolved, all units already renovated, average rents stabilized at around 1,550 dollars per month per unit, and lower rent growth, the decision was made to put the property up for sale.

After a few months, in which the main obstacle was the delay in granting the buyer's financing, the deal was closed for US$ 84 million, a 47% appreciation relative to the acquisition price of US$ 57.2 million. Considering these values and the property's Net Operating Income (NOI) in the 12 months prior to the sale, the transaction was carried out at a capitalization rate (cap rate) of 5%, demonstrating the resilience of the residential market even in a more challenging market moment.

Conclusion

The investment in the Park Crescent multifamily is a very interesting example of how it is possible to obtain good returns in the U.S. real estate market through careful property selection and active management of those properties. Thus, even with the pandemic and the worsening economic scenario, it was possible to renovate the property, improve management, increase profit and carry out a sale at a good price.

In this case, despite the more challenging moment for the economy, it is important that investors take into account the specific fundamentals of each local market and the dynamics of those markets, which tend to prevail over the national macroeconomic scenario. More than that, in moments of greater uncertainty, it is common for many opportunities to arise—whether because some sellers come under pressure, or because many buyers become reluctant to invest, reducing competition for good assets.